記住我

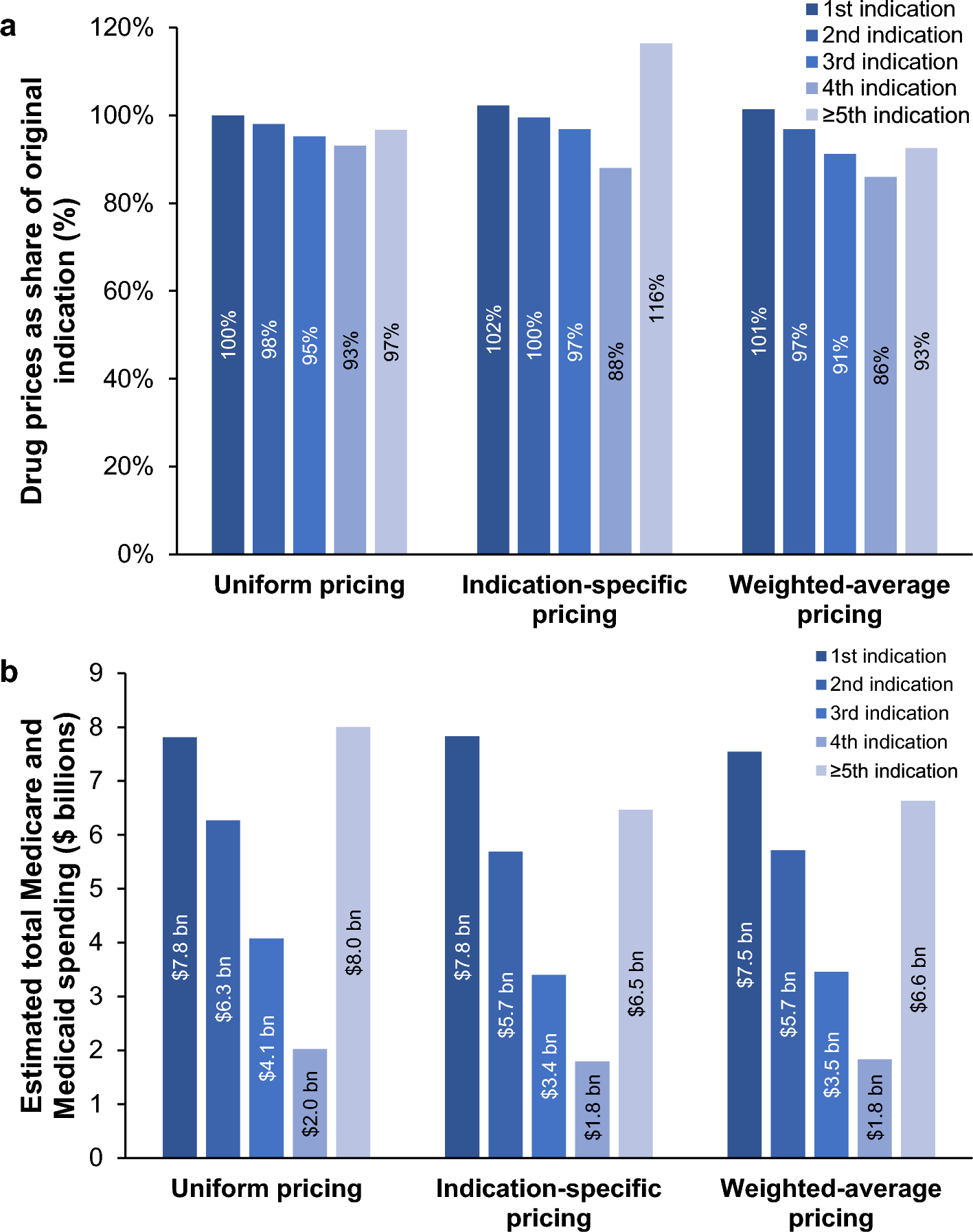

We estimate that Medicare and Medicaid could have realized cost savings of $3.0 billion (10.6%) with both value-based ISP or weighted-average pricing in 2020. These savings would be especially realized by reducing prices for low-value non-orphan follow-on indications for partial orphan drugs.

4.1 Value-Based Indication-Specific PricingWe estimated that value-based ISP would reduce Medicare and Medicaid spending on supplemental indication approvals, particularly for non-orphan indications of partial orphan drugs. This is especially desirable given that supplemental indications were shown to be of lower value to patients and insurers [1, 27, 28]. Furthermore, partial orphan drugs were criticized for benefiting from high orphan drug prices for their non-orphan indications, resulting in substantial revenues and profit streams for manufacturers [3, 5, 7]. ISP could resolve these disputes. However, confirming Chandra and Garthwaite’s theoretical expectations [12], ISP would also result in higher prices for patients who benefit most from new drugs, for example, patients with ultra-rare diseases. On the upside, pharmaceutical companies would be encouraged to especially develop high-value treatments for ultra-rare diseases. On the downside, this could lead to increased pharmaceutical expenditure in the long term. Moreover, the implementation of ISP remains challenging. It requires the tracking of drug usage across indications, which is currently not available across the entire USA. Given these technical challenges, alongside opposition from key stakeholders, scholars previously concluded that ISP is not feasible to implement (at least in the short term) [13].

4.2 Value-Based Weighted-Average PricingSimilar to ISP, the adoption of value-based weighted-average pricing would reduce Medicare and Medicaid’s expenditure on cancer drugs by 10.6%. These cost savings would be realized by sequentially lowering the drug’s initial list price as new supplemental indications receive FDA approval. These results are consistent with a prior study that showed cancer drug prices declined with the introduction of each new indication in Germany and France (countries that employ weighted-average pricing) [27]. In contrast to ISP, the adoption of weighted-average pricing does not increase but reduces prices for drugs treating ultra-rare diseases. Thereby, weighted-average pricing could help to improve the financial sustainability of costly ultra-orphan drugs.

Medicare and Medicaid should, therefore, carefully examine the mechanisms of a weighted-average pricing system for its price negotiations as part of the Inflation Reduction Act of 2022 [46,47,48]. Given that the Secretary of Health and Human Services will be allowed to directly negotiate prices of the top-grossing drugs with manufacturers, weighted-average pricing considerations could support price proposition for top-selling drugs with multiple indications, especially partial orphans.

Nonetheless, there are several barriers to implementing weighted-average pricing across the entire USA [9, 11, 19, 20]. First, it requires an understanding that drug prices can be negotiated between insurers and manufacturers based on their value proposition for patients (value-based pricing). Second, value or benefit assessments must be conducted for each additional indication that receives FDA approval. Thereafter, payers and insurers must set or negotiate a price for each indication. These indication prices are then combined with the anticipated or monitored indication usage to calculate a single drug price. Given that drugs are still sold for a single price under weighted-average pricing, it is more feasible than ISP to implement in the current US healthcare system. However, similar to ISP, politicians must propose changes to the current US drug price system and overcome opposition from pharmaceutical benefit managers, pharmaceutical companies, and other stakeholders that stand to lose with a new pricing policy.

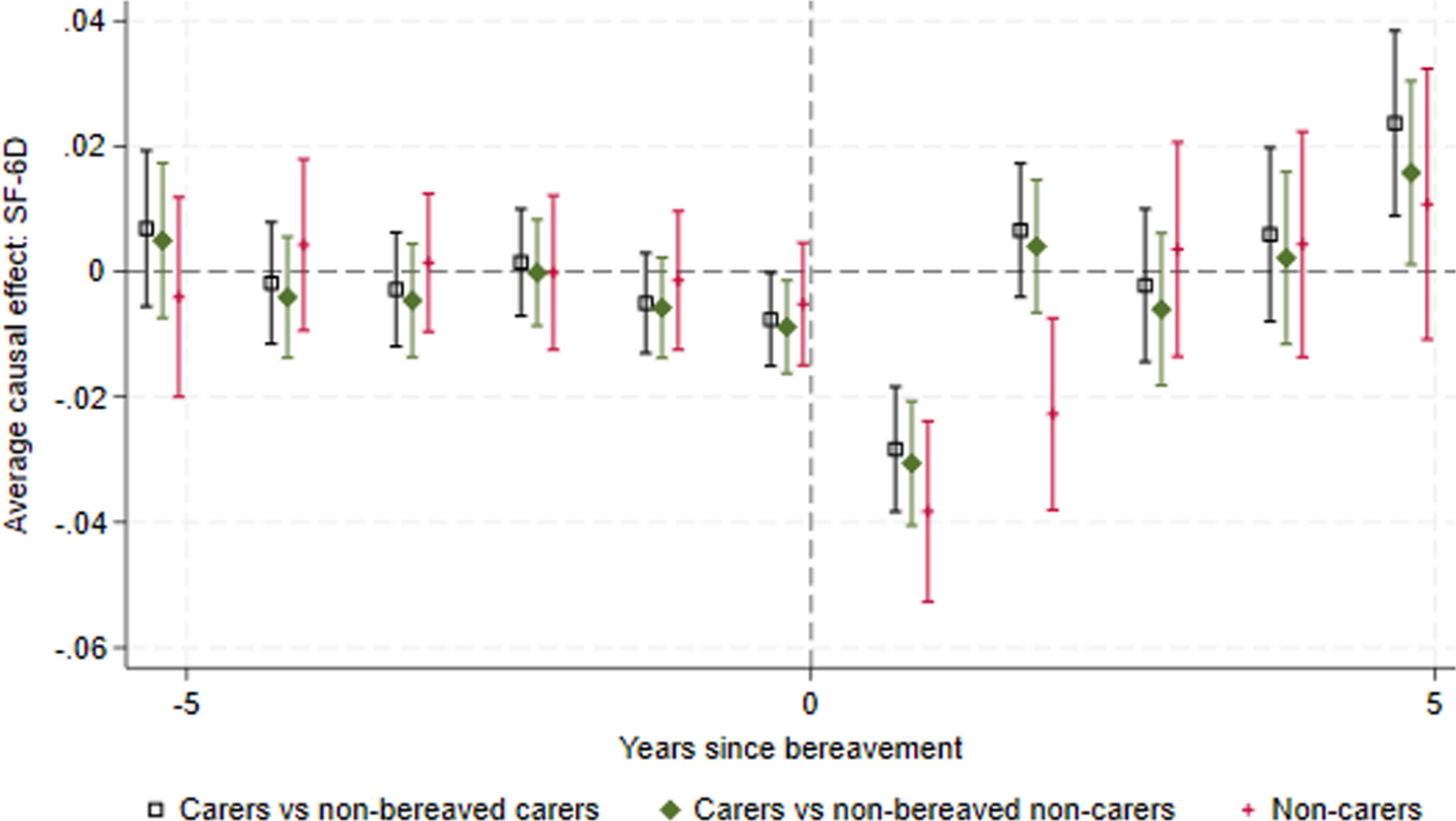

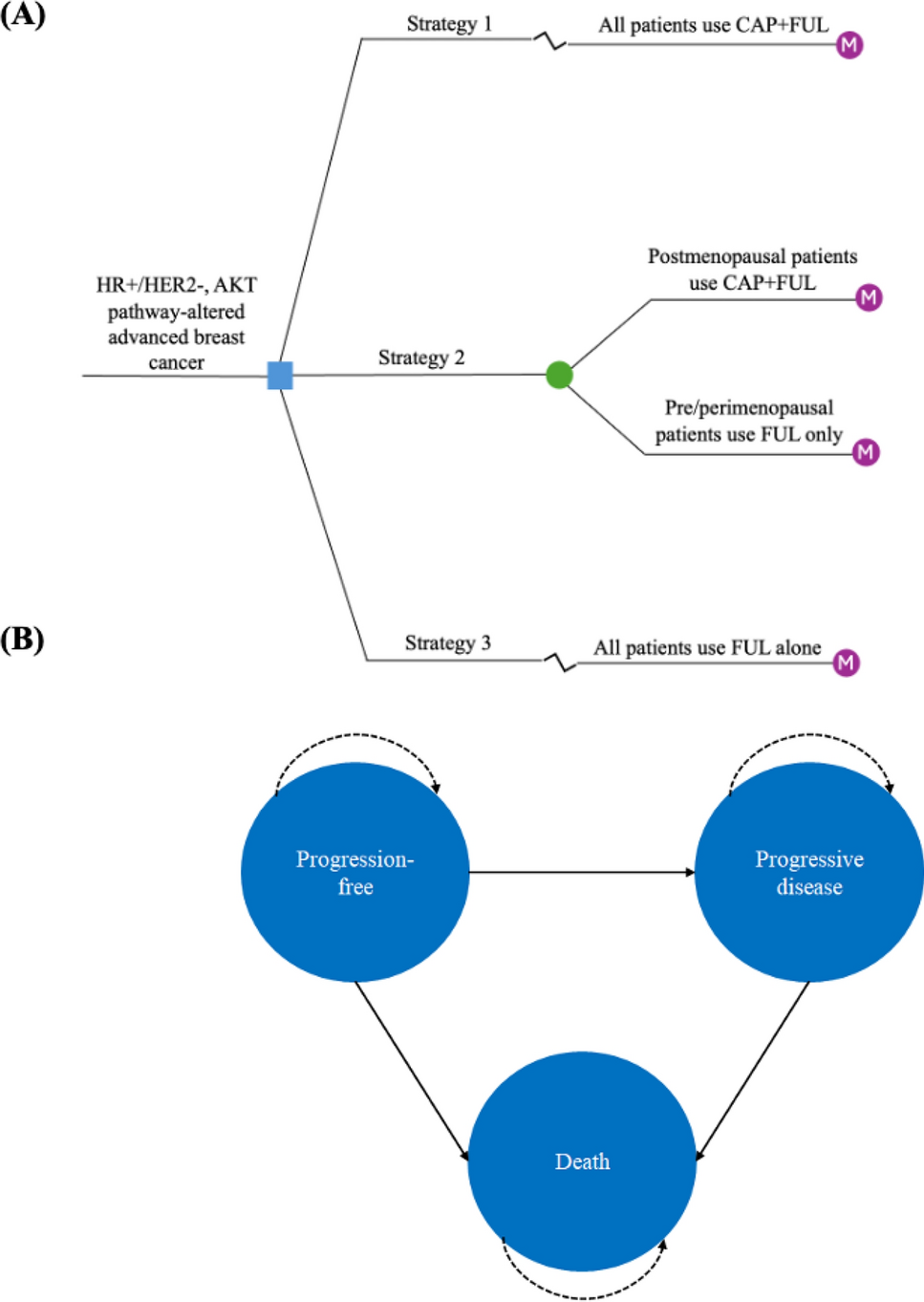

4.3 Short- and Long-Term Effects of Value-Based Indication-Specific PricingIn this study, we estimated static short-term price and cost savings for value-based ISP and weighted-average pricing. However, economists previously debated that the dynamic long-term economic effects of ISP on social welfare, consumer surplus, and producer surplus may differ (Fig. 2) [12, 21, 26, 49]. Bach [21], who assumed that US prices are set based on the first high-value indication (single-highest price), argued that ISP would increase patient access to new treatments, reduce prices for low-value indications, and, thereby, increase social welfare, payers’ spending and producer surplus (Fig. 2a). In contrast, Chandra and Garthwaite [12], who assumed that US prices are set based on the lowest-value indication (single-lowest price), argued that (overall) ISP would increase drug prices for high-value indications, increase payers’ spending, and transfer consumer surplus to producers while social welfare would remain constant (Fig. 2b). Similarly, a recent simulation study highlighted that ISP would reduce consumer surplus and thereby patient welfare relative to a single weighted-average pricing policy [50].

Fig. 2

Short- and long-term effects of value-based indication-specific pricing on consumer surplus, producer surplus, prices, spending, and social welfare. Under a single-highest list price scenario, producers only sell their drug at price PUh for the HV indication to NUh patients. Patients in the MV and LV indication may not have access to the drug because insurers are reluctant to reimburse drugs for a price exceeding the indication’s incremental value. In the short term, adopting indication-specific pricing would reduce prices, increase spending, increase patient access, increase producer surplus, and thereby increase welfare. Under a single-lowest list price scenario, producers sell their drug at price PUl to NUl patients with indications HV, MV, and LV. Adopting ISP would increase prices, increase spending, increase producer surplus, and increase welfare, and patient access would remain unchanged. In the long term, ISP encourages the development of new MV and LV indications. The dynamic market entry of new indications under this scenario, with fierce competition between these new indications, would lower prices for the MV and LV indications to PMVd and PLVd. Graphs adapted from Towse (2018) [26]. HV, high value; LV, low value; MV, medium value

Under a single drug price system, the adoption of value-based ISP encourages pharmaceutical companies to launch new low-value indications (Fig. 2c). Theoretically, with a single drug price, companies would be incentivized to withhold these indications as they would deteriorate this single price [27,28,29]. Similarly, insurers would be reluctant to reimburse indications for a price exceeding the indication’s incremental value. These additional new indication launches would increase patient access to new therapeutic options. This expanded access would, of course, increase consumer surplus and producer surplus and thereby maximize social welfare. In the short term, the additional approval of new indications would also increase payers’ spending. Nonetheless, this additional spending would increase enrollees’ health benefits, if ISP were to be adopted as part of a formal health technology assessment (HTA) process that uses value-based pricing. In a system with a formal HTA process, payers only reimburse new cost-effective indications, for example, indications with an incremental cost-effectiveness ratio below the nation’s willingness-to-pay threshold. A formal HTA process essentially ensures that pharmaceutical companies are only incentivized to develop new indications that are worthwhile for patients and the health system.

The long-term effects of ISP are more complex (Fig. 2d). As previously explained, pharmaceutical companies are incentivized to research, develop, and launch more indications under ISP. The increased number of new indications would likely intensify competition at the indication level. Economic theory suggests that the market entry of new competitors drives down prices, even below the national willingness-to-pay threshold [26]. These dynamic competitive effects of ISP could, thereby, increase consumer surplus, while reducing producer surplus and payers’ spending. However, previous studies analyzing brand–brand competition in the pharmaceutical market could not confirm that the entry of new competitors would result in a reduction in drug prices [25, 51]. Furthermore, our sensitivity analysis highlighted that the estimated cost savings are subject to consumers’ underlying PED. As a consequence, price reductions for low-value indications could increase consumer demand and thereby increase payers’ overall spending in the long term. On the other hand, a positive PED also implies that higher prices for high-value indications could pose a barrier for consumers to purchase drugs that deliver substantial value to them and, therefore, reduce spending (especially in the USA). Our analysis suggests that, because low-value indications are typically for diseases with a higher prevalence and high-value indications are typically for diseases with a lower prevalence, the effects of a positive PED would likely diminish the estimated cost-saving potential.

4.4 LimitationsThere are several limitations inherent to our analysis. First, our model did not capture the upfront investments and ongoing administrative costs of introducing ISP or weighted-average pricing. Presumably, the cost of introducing weighted-average pricing would be lower than that for ISP, given that the latter requires the introduction of new information technology and prescription systems across healthcare providers in the USA, whereas the former only entails a novel way to calculate, negotiate, and assign single drug prices. Furthermore, we only calculated cost savings for cancer drugs. Adopting a new pricing policy would, of course, also reduce costs for drugs of other therapeutic areas. This would also mean that upfront investments in introducing these novel pricing systems could be shared (and likely be easily covered by the savings realized) across all therapeutic areas. Second, we conducted a retrospective analysis. Cost savings that Medicare and Medicaid may realize in the future may differ. Nonetheless, our model highlights the mechanism of ISP and weighted-average pricing policies, particularly underlining their implications for partial orphan drugs and indications for ultra-rare diseases. Third, other pricing mechanisms, such as indication-specific discounts on drug prices, single-lowest drug prices, or indication-specific managed entry agreements, are currently employed in countries but not included in our analysis [9, 11]. Although these policies impact drug spending and usage, they do not affect list prices—the underlying main variable of our model. Fourth, our analysis was based on list prices without considering closely guarded confidential rebates/discounts. Results may therefore vary for net prices and patient out-of-pocket spending, although rebates and discounts are small for anticancer drugs [35]. Further, price and spending data were evaluated for Medicare and Medicaid. Within the heterogeneous US healthcare market, drug prices may substantially vary across insurers, states, and insurance schemes.

留言 (0)