According to the National Thalassaemia Registry and the local expert panel, 526 patients with transfusion-dependent β-thalassemia can be considered eligible to receive luspatercept. The patient pool is considered stable over the 5-year time horizon since the preventive measures have reduced the incidence of the disease.

In the scenario where a 40% dropout rate is assumed (Table 1), an incremental budget impact of €1,476,279 is forecasted in the first year following the introduction of luspatercept. This is expected to reach €6,309,351 by year 5 of luspatercept reimbursement. The annual cost following introduction of luspatercept is estimated at €18,538,390 in the first year and will escalate to €23,371,463 by year 5. The current scenario, where luspatercept is not reimbursed, assumes a steady expenditure of €17,062,111.

The total PMPY costs are estimated at €1.56 in first year and €6.68 by year 5. The PMPM costs are estimated at €0.13 in the first year and €0.56 by year 5.

The PTMPM costs are gauged at €233.88 in the first year and peak at €999.58 by year 5.

In the scenario where a 25% dropout rate is assumed (Table 2), an incremental budget impact of €1,845,312 is forecasted in the first year following the introduction of luspatercept. This is expected to reach €7,611,912 by year 5 of luspatercept reimbursement. The annual cost following introduction of luspatercept is estimated at €18,907,423 in the first year and will escalate to €24,674,023 by year 5. The current scenario, where luspatercept is not reimbursed, assumes a steady expenditure of €17,062,111.

The total PMPY costs are estimated at €1.95 in first year and €8.06 by year 5. The PMPM costs are estimated at €0.16 in the first year and €0.67 by year 5.

The PTMPM costs will begin at €292.35 in the first year and peak at €1205.94 by year 5.

Table 3 presents the budget impact of luspatercept reimbursement per year for both scenarios.

Table 3 Budget impact of luspatercept reimbursementIn terms of total budget impact, in the RWD scenario, the payer is anticipated to invest an additional 20% into the existing costs of thalassemia management over a 5-year period, solely for the introduction of luspatercept in the regimen. In absolute terms, this amount exceeds 21 million euro. The corresponding increase in the RCT scenario was estimated at 23%, which exceeds 25 million euro.

Regarding the overall expenditure over a 5-year period, we observed minor savings in RBCT and iron chelating agents’ costs centers attributed to luspatercept reimbursement. Nevertheless, these savings fall short of making up for the steep acquisition cost of luspatercept. This is further corroborated by the other BIA metrics such as PMPY, PMPM and PTMPY. Although no explicit threshold applies for Cyprus, these metrics can cumulatively complement the incremental budget impact, aggregating into an informed health decision making.

While all acquisition costs burden the payer, any potential savings achieved by a reduction of RBCTs will not be capitalized upon, as blood is considered a public good in Cyprus. Nevertheless, we consider that is necessary to calculate the potential savings and include them in the analysis, as the classification of blood as a public good does not render it cost-free.

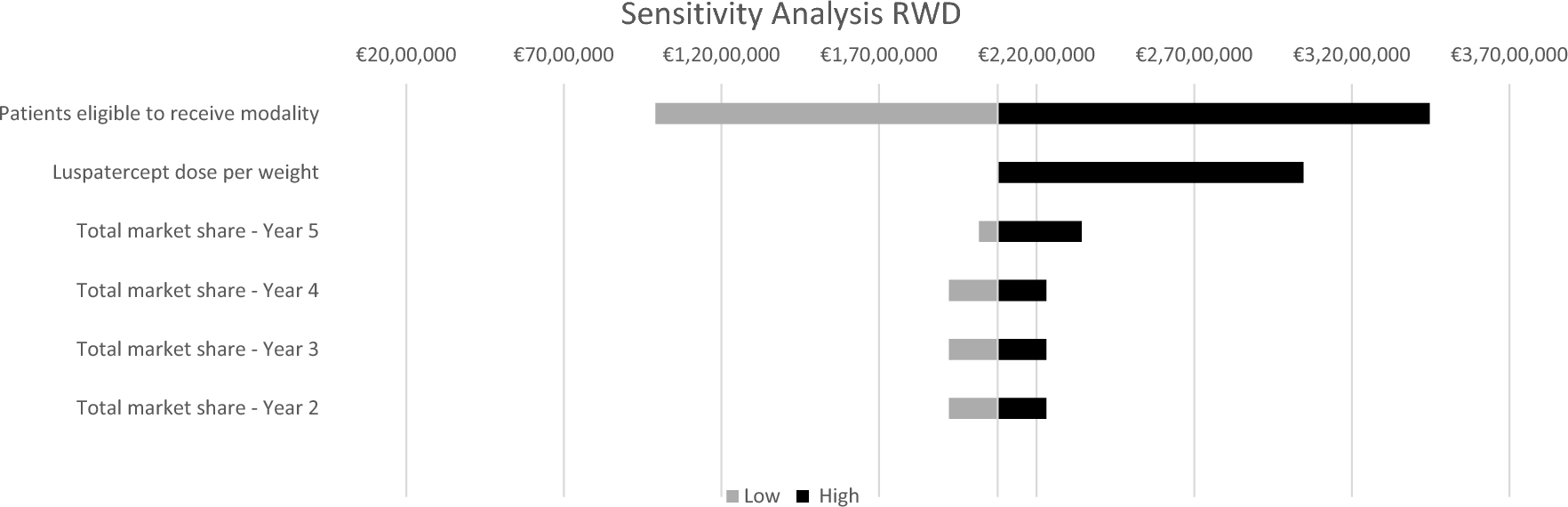

In addition to BIA, a deterministic sensitivity analysis was performed on both scenarios in order to elucidate the uncertainty encompassing model parameters.

According to the results of the sensitivity analysis, the main cost drivers for both scenarios were the number of eligible patients and the dose per weight. Since the number of eligible patients is only contingent to the reimbursement guidelines, the deterministic sensitivity analysis provides an appropriate backdrop to investigate the effect of model parameters on the total budget impact [24]. To this end, we decided to use a deterministic sensitivity analysis as we aimed to emphasize the quantitative relationship between changes in inputs and outputs [24].

Sensitivity analysis results for ‘Scenario RWD’ are presented in Fig. 1 and results for ‘Scenario RCT’ are presented in Fig. 2.

In our scenarios, we used the procurement prices of iron chelating agents. To balance out luspatercept’ absence of financial agreement, we assessed the budget impact of introducing luspatercept in a reimbursement model using the wholesale prices for all corresponding pharmaceuticals.

The weighted discount achieved among the iron chelating agents was 35%. Therefore, a 54% increase in the iron chelating agents’ prices indicates the expenditure of the therapies without financial agreements, based on wholesale prices.

The result of this change led to an anticipated total expenditure increase for the management of thalassemia. Nevertheless, the differences in incremental budget impact were barely distinguishable from the primary analyses. In the RWD scenario, the incremental budget impact changes from €21,300,643 to €21,114,336 (20% vs 17%). In the RCT scenario, the corresponding results are €25,834,368 vs €25,182,293 (23% vs 20%). This reinforces the robustness of the findings of the two primary scenarios regarding the modest effect of luspatercept on iron chelating agents’ utilization.

留言 (0)