記住我

This section describes GGFs’ investment in P&B, and factors influencing where, when and how they invest.

What do market data tell us?GGFs have invested in a wide range of industries, of which the most significant ones are strategic emerging industries. Semiconductors, electronics, P&B, and energy receive the most investment from 2000 to August 2021 (Fig. 2). The semiconductor industry has received extremely significant GGF investment, linked to competition between China and the US from 2018 (see discussion below). As a strategic emerging industry in China, the P&B sector has also attracted significant investment. Fig. 3 shows 1,328 investments, placing P&B second by number of investment cases, with a disclosed investment over RMB 42.1 billion (about USD 6.5 billion), rating 4th in overall volumes of investment. GGFs’ activity in this sector began to rise in 2015, increased sharply in 2017, and peaked in 2020.

Fig. 2

GGFs’ investments by cases and size in different sectors from 2000 to August 2021 Source: Authors’ analysis of data from PEDATA

Fig. 3

GGFs’ investments in P&B from 2000 to August 2021 Source: Authors’ analysis of data from PEDATA

Fig. 4

Investment stages of GGFs in P&B by case from 2000 to August 2021 Source: Authors’ analysis of data from PEDATA

Our data show that oncology and chronic disease therapies receive the most funding from GGFs among all new medicine pipelines in the P&B sector. However, potentially less commercially lucrative pipelines, such as antimicrobials and anti-infective drugs, and vaccines for communicable diseases, have attracted little funding. Only 28 investments have been made into such pipelines out of 420 disclosed investments in new medicine pipelines, or approximately 7%. This result is contrary to our expectations, given the stress in both national and local policiesFootnote 2 on the need to prioritise R&D with a social purpose and for new medicines that meet a social need. Our data, however, do not show GGFs prioritise such investments in their portfolios.

GGFs’ investments also differ by the stage of development of companies they invest in. Fig. 4 shows that GGFs’ investments are concentrated in companies in the expansion stage, with less invested in companies in early stages. Such investments have grown significantly more than investment in start-ups and mature companies, and seed-stage companies continue to be left behind.

How to understand GGFs investments in P&B?After mapping investments in the P&B sector, we interviewed GGF executives and managers and explored how they understand investing in P&B. Three main themes emerged from the interviews and are discussed here: that GGFs investments in different sectors respond to government policy; that specific government priorities in P&B help determine the focus of investments; and that GGFs tend to be late-stage investors, limiting their support to innovation.

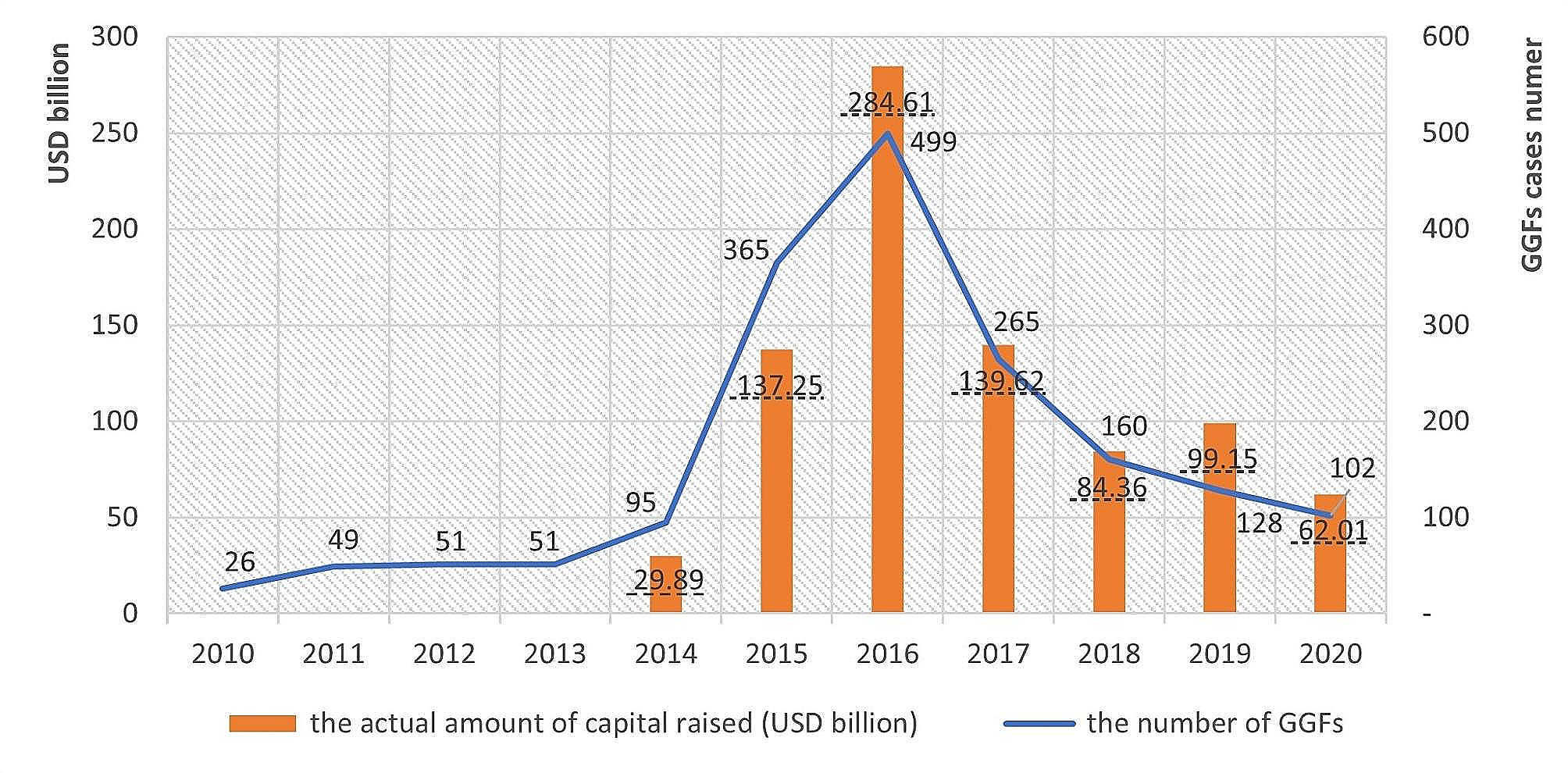

GGFs’ investments are responsive to changing government policyExisting literature points to P&B investments in China being highly policy-sensitive [53], and our interviewees (D, F, Q) argue that changes in industrial policy priorities have been the key determinant of GGFs’ investments in P&B in the last decade. On the advice of our interviewees, we compared the overall trend in GGFs’ investments with the trend of their investments in P&B and find that they differ. While the number of GGFs increased in 2015 (Fig. 5), their investments in P&B did not change significantly. Instead, P&B saw dramatic growth in 2017 (Fig. 6), as GGFs, overall, started to plateau.

Fig. 5

GGFs’ investments from 2014 to August 2021 (USD million) Source: Authors’ analysis of data from PEDATA

Fig. 6

GGFs’ investments in P&B from 2014 to August 2021 Source: Authors’ analysis of data from PEDATA

According to our interviewees, this reflects changes in government policy priorities for P&B, including the release of a national policy identifying P&B as a priority industry [56], and subsequent reforms, including dynamic updating of the National Reimbursement Drug List (NRDL), accelerated marketing authorisation of innovative drugs, and reforms to the hospital payment system.Footnote 3 These coordinated reforms reflect a strategic, coordinated, and mission-driven approach to development of the sector. This has started to create new markets for pharmaceutical companies, especially innovative drug developers (for example, sales of Herceptin and Avastin have increased substantially following inclusion in the NRDL [57] and have directly stimulated investment in the pharmaceutical sector (interviewee Q; 58).

GGFs’ investments are in line with government’s priority sectors – and market demandAll interviewees acknowledge that industrial policies guide GGFs’ investments. A recent high-level policy on priorities for development of P&B in China [56] provides technical guidance on developing new drugs, vaccines, and essential drugs for which there is an unmet clinical need. National and local industrial policies prioritize new drug development in the areas of oncology, cardiovascular diseases, diabetes, neurodegenerative diseases, psychiatric diseases, highly prevalent immune diseases, major infectious diseases, and rare diseases [56]. In practice, sub-national governments introduce industrial policies based on local conditions and in line with national policy [58, 59].

GGFs’ perceptions of the priorities of pharmaceutical and biotechnological industrial policies lead them to mainly concentrate their investments in oncology and chronic disease drugs (interviewees B, D, F, P, R). Interviewee F explains the rationale for investing in oncology drugs: not only is there potentially high demand if the drug is successful, but such investments are likely to receive national and/or local government support (to clinical trials, registration, and commercialisation), and follow on funding is likely to be easier to get, should it be needed. This shows how policy and market demand are frequently linked, including in national P&B policies, which stress the importance of clinical need [56]. Moreover, although GGFs are not required to make great profit, executives and managers have a default understanding that GGFs should not lose money A, B, F and O), leading to GGFs favouring new drugs viewed as policy priorities, as having potential high-demand, and being potentially profitable.

When we probed interviewees as to why few investments are made in antibiotics, or other pharmaceuticals with a ‘public goods’ character, informants told us that they have not really considered this issue or rarely receive business plans for antibiotics or similar drugs. Counterintuitively, despite the national level, strategic, target to develop new antimicrobials, evidence from our interviews shows this is not viewed as a policy priority by GGFs.

GGFs’ risk aversion and limited talent pool skew them towards later stage investmentsGGFs come in different kinds: start-up guidance funds, industrial guidance funds, and public-private partnership funds [60]. Of these three types, industrial guidance funds predominate. Such funds focus on industrial upgrading and development rather than supporting start-ups, which is likely to explain why there is limited early-stage investment. In P&B, this tendency reflects the risks of failure in the early stages of drug development, and the absence of ‘fault tolerance’ mechanisms, which limit GGFs’ appetite for risk (interviewees A, B, D, E, H, I, N, P). In P&B, most GGFs are therefore de facto ‘non-early stage’ funds (interviewee D), despite the policy intent behind them, which clearly includes support for innovative activities and early-stage investment, which is insufficiently provided by the private sector. Despite the evidence showing that GGFs can support innovation, therefore, there are likely to be limits to how this applies in P&B.

An insufficient talent pool is another constraint to GGFs supporting early-stage companies or programmes. Investing in P&B innovation requires professional staff with both an industrial background and knowledge of investment practice. However, competent professionals usually work for top international investors, rather than for GGFs (Interviewee B), and most GGF staff lack medical or biotechnology knowledge (interviewees B, C, F, Q, R). This appears to be a critical issue affecting the role GGFs can play in supporting innovation in P&B (see Sect. 4.2).

SummaryOur interviews show that while industrial policies play a vital role in GGFs’ decision-making in P&B, the drivers of GGFs behaviour are nuanced. They do not invest solely based on policy signals, but also assess the extent to which there will be a market for a given drug, whether because it aligns with China’s disease burden and public demand, or because of ‘pull incentives’ created through adjustments to government purchasing and reimbursement lists. In addition, our interviews show that there is, at best, a very weak policy signal coming through regarding the need for investment in companies developing antibiotics or bringing them to market. There are also concerns about GGFs’ capacity to really play the role as an early-stage, risk-taking investor, given their capacity constraints and absence of fault tolerance mechanisms. This, and GGFs’ having to balance an industrial development mandate with a profit motive, highlights a contradiction in how GGFs operate and their potential contribution in P&B.

GGFS’ potential to contribute to mission-driven innovation in P&BThe last section shows that GGFs face a variety of structural constraints in supporting innovation in P&B, including for products where there is a limited market – such as antimicrobials – even if these are a policy priority or of social importance. In our interviews, we wanted to more fully explore GGFs’ potential role in supporting ‘mission-driven’ R&D in P&B, given China’s willingness to use a range of industrial policy tools to support innovation and strategic industrial development, its increasing importance in P&B, and the government’s stated desire for China to play a larger role in supplying global public goods for health.

Our interviews therefore explored elements of mission-driven innovation and the extent to which GGFs align with, or support, the functions of this. This section discusses findings in three areas we probed with interviewees: whether GGFs should be understood as having a ‘social’ mandate in the way they approach investment decisions; their role in setting the direction of industrial development; and their role in creating and shaping markets. The section concludes with a discussion of some limitations of GGFs in supporting mission-driven innovation.

How should we interpret the social function of GGFs?The concept of mission-driven innovation includes the requirement that government help set the direction of development in line with social goals. To better understand how this function is operationalised through GGFs, we reviewed policy and literature on the purpose and functioning of GGFs, and questioned our interviewees regarding their understanding of the mandate of GGFs in promoting social goals, including – as in our study – pharmaceuticals such as antimicrobials that have characteristics of a ‘public good’ or ‘merit good’.

Our review is inconclusive. Policies frequently state the requirement that GGFs address systemic bottlenecks to industrialisation and development, but this requirement is unspecific. Meanwhile, our interviews show a lack of clarity over GGFs’ social mandate, that different groups may understand this differently, but that policy changes may be promoting an increase in the social component of GGFs’ mandate:

A number of GGF executives closely connected to government argue that GGFs should, de facto, be considered an extension of government because they are government-funded and -mandated (interviewees E, H, O, P and R), and that this gives them a composite responsibility, of promoting economic development and creating social benefit. They state that policies are being adjusted to give GGFs a more explicitly social mandate: a recent Ministry of Finance policy [61], for example, calls for GGFs to focus on ‘key and innovative sectors that require government intervention’ and ‘areas in urgent need of economic and social development’ [emphasis added]. This is leading some GGFs to change their operations, though GGFs still need to ensure profitable operation to be sustainable (interviewee P).

The views of managers, responsible for making operational decisions, differ from the first group, viewing GGFs as having only an indirect social mandate. These managers predominantly state that government should support social goals through taxation and subsidies, and that GGFs can contribute through promoting growth, tax revenues, and improving the government’s capacity to invest in such social goals (interviewees C, D, F, J, K and M).

How do GGFs articulate ‘directionality’ to help achieve social priorities?‘Directionality’ is a fundamental feature of mission-driven approaches to innovation, through which social purpose is articulated and translated into actions that can direct innovation towards that purpose. In this paper, novel antimicrobials are an example of an under-supplied pharmaceutical, which nevertheless serves an important social function. The interviews indicate two main ways in which GGFs can contribute to establishing the direction of innovation, though neither is fully exploited in the way GGFs currently function.

Setting GGFs’ investment focus. All interviewees confirmed that the government decides the investment focus of a GGF when it is established, and that other actors have little influence in this. This shapes subsequent investment behaviour and is therefore the most significant moment at which government influences a fund’s behaviour. For example, the scope of a fund could be defined as ‘advanced pharmaceutical and biotechnology technologies’ or, in more detail, as focusing on a specific disease or category of disease, such as ‘new oncology drugs’.

Setting GGFs’ investment stage. As discussed above, the stage at which a fund invests influences the extent to which it can support innovative technologies, and GGFs tend to make late-stage investments. In the P&B sector, a mature company is viewed as one that has completed drug discovery, received approvals to start clinical trials, or even entered Phase II trials (interviewees B, F, P, Q and R). Interviewees state that GGFs’ investment in P&B is changing rapidly, following COVID and changing government guidance (interviewees F, Q, R).Footnote 4

In other words, government has levers through which it is able to influence GGFs’ behaviour, and GGFs’ responsiveness to policy indicates that changing policies have the potential to change their investment focus. The change in focus following COVID-19 is to be expected, as government increasingly realises the strategic and social importance of P&B.

Market creation and shapingMarket creation and shaping is a core part of mission-driven approaches to innovation, reflecting the ‘joined up thinking’ that such approaches call for. An example is the use of purchasing mechanisms to stimulate the development of innovative pharmaceuticals (as in China’s NRDL), or to compensate for insufficient market demand in the case of antibiotics. While GGFs do not directly shape markets, they can be responsive to market-shaping efforts.

GGFs’ understanding of market potential as a driver. Our interviewees did not explicitly distinguish between drugs with a public goods character and for which there is insufficient demand, such as antibiotics, and others. On the contrary, they argued that potential market size is key to whether GGFs would invest in a given innovative drug (interviewee F, L, P and Q), as well as a drug’s clinical effectiveness, whether first-in-class or me-too (interviewee F and Q).

Probing antibiotics more specifically, interviewees argued that China’s large population base may provide a sufficient market even for drugs such as antibiotics (interviewee L and Q), whose use must be carefully stewarded, especially if they were included the NRDL (interviewees B, D, J, K, L, P and Q). This is echoed by a report from one innovative Chinese antibiotic developer [62]. This is a curious finding, but is likely related to an insufficient understanding of the need for stewardship of novel antimicrobials.

Strong industrial policies. In addition to the discussion above of the importance of policy direction in P&B, almost all our interviewees mentioned changes in the semiconductor sector to underline the importance of policy in shaping GGFs’ behaviour and aligning it with national priorities. Prior to the US ban on technology exports to China, investments in this sector were limited.Footnote 5 However, starting with the US-China dispute, Chinese industrial policy was rapidly adjusted, and investment by government and GGFs rose rapidly and dramatically, with the aim of substantially increasing China’s share of global chip manufacturing, complemented by the likelihood of growth in domestic demand for Chinese-produced chips.Footnote 6

Factors limiting GGFs contribution to social goals and public goods in P&BOur interviews explored factors that may impede GGFs from playing a larger social role and contributing to the development of pharmaceuticals with a public goods character, such as antimicrobials. This section synthesises the main factors stressed by our interviewees.

Insufficient talent pool. Section 3 notes that a limited talent pool is a constraint to GGFs’ investing effectively in P&B. Funds struggle to offer competitive income to attract qualified and competent staff (interviewees B, D, F, G, H, J, O, P, Q). The development of novel antimicrobials illustrates this – this requires highly specialised knowledge, especially given trends towards use of artificial intelligence (AI) in new antibiotic R&D [63, 64]. GGFs face great challenges hiring staff able to effectively assess such technologies and companies.

Insufficient fault-tolerance mechanisms. As discussed above, fault tolerance mechanisms reduce GGFs’ willingness to invest in risky, but potentially important, technologies and companies. This is despite high-level government policy stating the need for such mechanisms [65].

A third constraint is the absence of demand-creation mechanisms that could complement the supply-side support that GGFs are, in theory, able to provide to the development of public goods such as novel antimicrobials. In the case of antimicrobials, such mechanisms are very new, and currently only being trialled in a handful of cases [10].

留言 (0)