記住我

The healthcare insurance system is a significant institutional arrangement aimed at safeguarding the health of residents, enhancing their wellbeing, and maintaining social harmony and stability. Especially in rural areas of developing countries, the level of healthcare for the population is relatively inadequate. In 2003, China officially launched the New Rural Cooperative health insurance System (referred to as “New Rural Cooperative health insurance”), gradually establishing a basic health insurance system for rural residents. In 2007, the Urban Resident health insurance System, primarily targeting urban informal workers, was also established, further expanding the scope of China's health insurance system. Since 2011, more than 95% of the population in China has been covered by basic health insurance. The development direction of the basic health insurance system has shifted from achieving universal coverage to ensuring fairness. However, long-standing urban-rural development disparities persist, and the contradictions within the urban-rural divide have become more pronounced during the rapid urbanization process. Differences in the design of urban and rural social security systems have greatly affected rural residents' access to medical services and healthcare. This misalignment goes against the socialist goal of promoting equal access to public services and is particularly evident in the significant disparities that still exist between the New Rural Cooperative health insurance and Urban Resident health insurance systems in terms of medical benefits. These two systems are relatively similar in terms of funding mechanisms and institutional design, providing a strong foundation for further integration.

In 2016, the State Council of China issued the “Opinions on Integrating the Basic health insurance Systems for Urban and Rural Residents,” which called for the accelerated integration of the Urban Resident Basic health insurance and the New Rural Cooperative Medical Care schemes, aiming to establish a unified basic health insurance system for both urban and rural residents. By unifying coverage, financing policies, benefit packages, the health insurance catalog, designated healthcare providers, and fund management, the goal is to achieve integrated management and services for both urban and rural resident health insurance. This will significantly improve the health insurance benefits for rural residents and is expected to enhance their overall health status. Rural older people individuals represent one of the economically most vulnerable groups, concurrently lacking older people care, medical, and caregiving services, which makes them highly susceptible to issues such as “impoverishment due to illness” and “returning to poverty due to illness.” The health status of this demographic has become crucial for rural labor force development, rural industrial revitalization, and social stability.

The Health Capital Demand model, originally formulated by Grossman, posits that individuals' demand for medical services is derived from their demand for health (1). Health insurance alters the price of medical services when individuals require them. A reduction in the price of medical services stimulates their utilization, and it is undeniable that an increase in the utilization of medical services has a positive impact on health promotion. However, early studies on the impact of health insurance on health in China yielded inconsistent results. For instance, in their analysis of urban residents in the year 2000, Zhao and Hou found that the presence or absence of health insurance did not have a significant effect on health (2). Huang and Li conducted studies in 2002 and 2005, which indicated that health insurance promoted the health of older people individuals (3). The differing results could very likely be attributed to the early stage of the health insurance system's establishment at that time, where the health effects might not have been evident yet, along with differences among the study populations. Furthermore, there is not a complete consensus within the academic community regarding the health improvement effects of the New Rural Cooperative Medical Scheme (NRCMS). Lei and Lin found that the New Rural Cooperative Medical Scheme (NRCMS) had no significant impact on the health of farmers (4). However, the results of Wu and Shen's study indicated that the NRCMS system had a positive influence on the health improvement of farmers (5). Since 2016, China has undergone a large-scale integration of urban and rural residents' health insurance, merging the New Rural Cooperative Medical Scheme (NRCMS) and the urban resident health insurance system. This integration has effectively increased the health insurance benefits for rural residents. Research on the impact of health insurance on health has evolved from examining whether residents have health insurance to assessing the influence of improvements in health insurance benefits (6). Some scholars have already examined the impact of the integration of urban and rural resident health insurance on health. Studies by Zheng et al. and Tan and Cao both indicate that the integration of urban and rural resident health insurance can enhance the utilization of medical services among the insured population, thereby promoting health (7, 8). Hong et al. went further to demonstrate that the integration of urban and rural resident health insurance not only promotes health but also reduces health losses among rural middle-aged and older people individuals (9).

However, most previous studies have typically chosen one or a few indicators among self-rated health, mental health, or cognitive impairment. While these indicators can provide relatively detailed insights into the impact of various factors, both subjective and objective, on different health states, they may not comprehensively reflect the overall health status of middle-aged and older people individuals. Secondly, previous research on the impact of health insurance, including New Rural Cooperative Medical Schemes (NRCMS) and urban-rural resident health insurance (URRMI), on health has often assumed that the effects of health insurance on middle-aged and older people individuals with different health statuses are homogeneous. However, with the increase in reimbursement rates, the impact of health insurance on the health of critically ill patients may be more significant. This is because the current health insurance system in China primarily focuses on catastrophic illnesses, particularly those requiring hospitalization, and provides additional medical assistance policies for patients with extremely severe illnesses. Moreover, the higher reimbursement rates mean that critically ill patients will receive larger compensation amounts from health insurance policies. Consequently, the marginal effect of health insurance on their health improvement will be greater. Previous research has often overlooked the heterogeneity in the impact of urban-rural resident health insurance integration on health improvement among individuals with different health statuses. Importantly, as individuals enter middle and old age, their health tends to decline significantly, and there are greater variations in the health status of different middle-aged and older people individuals. Examining the effects of urban-rural resident health insurance integration on individuals with varying health statuses can facilitate the development of more precise healthcare policies tailored to patients with severe illnesses.

2 Theoretical analysisGrossman introduced the concept of health capital and developed a health demand model (1). In this model, it is assumed that consumers' demand for medical services is driven by their demand for health (1). Assuming a representative consumer's utility function at different stages of life is:

U=U(ϕtHt,Zt),t=0,1,…,n (1)Ht represents the stock of health capital, while Zt represents the quantity of goods other than health. Consumers face two types of constraints when making investment decisions: one is the income constraint, as in traditional consumer theory, and the other is the time constraint. The budget constraint that consumers face is given by:

∑t=0nPtMt+QtXt(1+r)t=∑t=0nWtTWt(1+r)t+A0 (2)Pt and Qt represent the prices of medical services (Mt) and other commodities (Xt), respectively. Wt denotes the wage rate, TWt signifies working hours, and A0 represents the initial wealth. In addition to the budget constraint, consumers also face a time constraint:

TWt+Tht+Tt+TLt=Ω (3)Where TWt represents working time, TLt signifies time lost due to poor health, Tt stands for the time allocated to producing goods, and Tht represents time invested in health improvement. The equilibrium conditions for the above model are derived as follows:

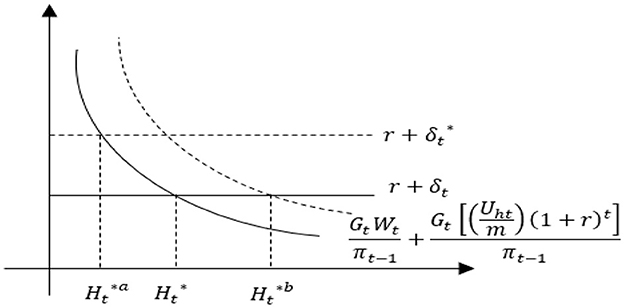

γt represents the market rate of return on health as an investment, αt represents the marginal utility value of health when it is consumed as a good. This is often referred to as the consumer's psychic return rate. r represents the interest rate, δt represents the depreciation rater. As illustrated in Figure 1, the intersection of the benefit curve and the cost curve for health determines the optimal demand for health, denoted as Ht*. We simplify health investment as the utilization of medical services. In this case, if the cost of utilizing medical services decreases, it will only reduce the marginal cost of health investment (πt − 1). The benefits curve, derived from γt=WtGtπt-1 and αt=Gt[(Uhtm)(1+r)t]πt-1, will shift to the right, leading to an increase in the consumer's optimal demand Ht* for health. The increase in health demand results in higher utilization of medical services by the consumer.

Figure 1. Comparative statics analysis of health demand.

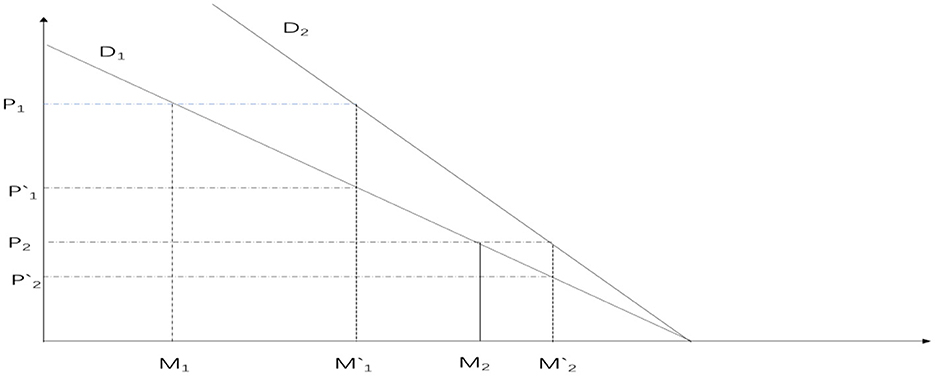

The promotion of health through increased utilization of healthcare services is unquestionable (7, 8, 10). As deduced from the previous Grossman model, healthcare services are considered normal goods. When the price of healthcare services (P) decreases, it implies a reduction in the marginal cost of health investment, thereby increasing the marginal return on health. Hence, consumers' demand for health and medical services will increase. Under the original coverage of the New Rural Cooperative Medical Scheme (NRCMS), the slope of the consumer's medical demand curve is negative, as represented by the D1 line in Figure 2. Assuming that the integration of health insurance reduces the price consumers face when seeking medical care from P1 under the NRCMS to P‘1 under the integrated urban and rural resident health insurance, consumers' demand for medical services will increase from M1 to M‘1. This change can be illustrated in Figure 2 by the shift from the original D1 to the new D2 curve. In other words, the improvement in health insurance benefits, leading to a decrease in the actual price consumers pay for medical services during treatment, will naturally increase the demand for medical services, thereby promoting health. From a practical perspective, the integration of urban and rural resident health insurance can improve the health status of rural residents, after the integration of urban and rural resident health insurance, the reimbursement rate for rural residents' medical expenses will increase. Taking the example of the inpatient reimbursement rate, which undergoes the most significant change, the reimbursement rate for hospitalization expenses within the payment policy scope of New Rural Cooperative Medical Scheme (NRCMS) is ~56.6%, while the reimbursement rate for hospitalization expenses within the payment policy scope of urban and rural resident health insurance is about 69.3% (11, 12).

Figure 2. The impact of health insurance system on consumer medical demand curve.

Furthermore, during the transformation from New Rural Cooperative Medical Scheme (NRCMS) to the Urban and Rural Resident health insurance (URRMI), this process may have heterogeneous effects on the health of middle-aged and older people individuals with varying health conditions. Middle-aged and older people individuals, due to the aging process, often experience a significant decline in their health compared to when they were younger. Moreover, because of differences in long-term health accumulation, there are substantial variations in health among this population. Individuals with different health statuses tend to have different types of illnesses, and the medical expenses incurred when seeking healthcare also vary. Relatively speaking, individuals with poorer health are more likely to develop severe illnesses, resulting in much higher medical expenses compared to those with milder health conditions. Furthermore, health insurance reimbursement rates do not decrease as medical prices increase. On the contrary, China's existing health insurance system often includes supplementary insurance for severe illnesses for individuals with significant healthcare needs. Urban and rural catastrophic illness insurance is designed to reimburse urban and rural residents for the substantial medical expenses incurred due to severe illnesses. Its primary goal is to prevent urban and rural residents from facing catastrophic medical expenditures. The insurance system establishes payment ratios segmented based on the level of medical expenses. In principle, as medical expenses increase, the payment ratio also increases, effectively minimizing the personal financial burden of medical costs. This, in turn, further elevates the reimbursement rates for individuals with severe illnesses, alleviating concerns about the high cost of healthcare and encouraging them to seek medical treatment.

Moreover, the medical services required by patients with severe illnesses are usually much more expensive than those for individuals with milder conditions. As depicted in Figure 2, the medical price for patients with severe illnesses is represented as P1, while for patients with milder conditions, it is P2. After the integration of health insurance, the reimbursement rates become P‘1 and P‘2, respectively. However, the change in optimal medical services for patients with severe illnesses (M1‘-M1) is significantly greater than that for patients with milder conditions (M2‘-M2). This implies that the impact on the health of patients with severe illnesses is greater, aligning with the primary function of health insurance to “protect against major illnesses.” Based on this, we propose the hypothesis:

Hypothesis: The integration of urban and rural resident health insurance can promote the health of rural middle-aged and older people individuals, with a greater impact on those with lower health levels.

3 Data source and research methods 3.1 Data sourceThe data used in this study is sourced from the China Health and Retirement Longitudinal Study (CHARLS). CHARLS is a large interdisciplinary survey project conducted by the National School of Development at Peking University, in collaboration with the China Social Science Survey Center at Peking University and the Beijing University Youth League Committee. It primarily focuses on individuals aged 45 and above. The baseline survey of CHARLS in China was conducted in 2011, with follow-up surveys conducted every 2–3 years. Considering that the integration of rural and urban resident health insurance systems took place gradually in different regions, the large-scale integration of the New Rural Cooperative Medical Scheme (NRCMS) and the Urban Resident Basic health insurance (URBMI) into the Urban and Rural Resident health insurance (URRMI) occurred in 2016 following the issuance of the State Council's “Opinions on Integrating the Basic health insurance Systems for Urban and Rural Residents.” The policy impact primarily occurred between 2015 and 2018. Based on this, this study utilizes the most recent data from the 2015 and 2018 waves of CHARLS.

3.2 Variable selection 3.2.1 HealthHealth is commonly defined as a state of complete physical, mental, and social wellbeing and not merely the absence of disease or infirmity. Health is the foundation of human survival and development, serving as not only a prerequisite for survival but also as the basis for realizing individual potential and pursuing happiness. To address the limitations of traditional health measurement indicators, many scholars in recent years have used frailty indices to reflect the health and aging status of middle-aged and older people individuals (13, 14). The frailty index (FI), also known as the health deficit index, refers to the proportion of health measurement indicators for which an individual's value is considered unhealthy. It has a range of values from 0 to 1, with a higher frailty index indicating poorer health. This study comprises the following six modules:

(1) Self-rated health (HEALTH): How do you rate your health? Define it as 0.2 for “very good,” 0.4 for “good,” 0.6 for “fair,” 0.8 for “bad,” and 1 for “very bad.”

(2) Instrumental Activities of Daily Living (IADL): Do you have difficulty with “managing money, shopping, cooking, making phone calls, and housekeeping?” If you have difficulty, define it as 1, otherwise as 0.

(3) Activities of Daily Living (ADL): Do you have difficulty with “bathing, getting out of bed, using the toilet, eating, dressing, and making decisions?” If you have difficulty, define it as 1, otherwise as 0.

(4) Functional Limitations: Do you have difficulty with activities such as “walking 100 m, climbing stairs, reaching up, getting up from a chair, bending or kneeling or squatting, picking up a coin, carrying a 10-kg weight?” If you have difficulty, define it as 1, otherwise as 0.

(5) Mini-Mental State Examination (MMSE): Can you clearly answer, “What year is it? What month is this? What is the date today? What season is it now? What day of the week is today? How is your memory right now? Can you draw the picture you see? And what is your level of depression?,” Memory, similar to self-rated health, is defined as follows: “very good” is defined as 0.2, “good” as 0.4, “fair” as 0.6, “bad” as 0.8, and “very bad” as 1. All other responses are correctly defined as 0, and any other answers are defined as 1.

(6) Chronic diseases, based on whether one has them or not, including conditions like hypertension, hyperlipidemia, hyperglycemia, malignant tumors, chronic lung diseases, liver diseases, heart diseases, stroke, kidney diseases, gastrointestinal diseases, emotional and mental issues, memory-related diseases, rheumatism, and asthma, are defined as 0 (absent) or 1 (present).

The above-mentioned six modules collectively involve 41 health variables, with specific formulas as follows:

In the above formulas, FI represents the frailty index, with n = 41, and di = 1 indicates that the i-th health variable is in a compromised health state; otherwise, di = 0. The frailty index is a continuous variable ranging from 0 to 1, where a higher frailty index indicates a poorer health condition of the surveyed individuals.

3.2.2 The integration of urban and rural residents' health insuranceFirst, individuals who participated continuously in both 2015 and 2018 were selected. This includes individuals who were enrolled in the New Rural Cooperative Medical Scheme (NCMS) in 2015 and remained enrolled in the NCMS in 2018, as well as individuals who were enrolled in the NCMS in 2015 and switched to the Urban and Rural Resident Basic health insurance (URRBMI) in 2018. Individuals' participation in the integrated Urban and Rural Resident Basic health insurance (URRBMI) can be identified based on their responses regarding the type of health insurance they had (6, 15–17). This information can be used to determine whether they experienced the integration of rural and urban resident health insurance schemes. To mitigate the possibility of rural middle-aged and older people individuals being uninformed about this policy due to information gaps, a household-based approach was adopted to ascertain their insurance participation status. If at least one member within their household had undergone the integration of Urban and Rural Resident Basic health insurance (URRBMI), then the rural middle-aged or older people individual was considered to have experienced the integration of URRBMI. Furthermore, we conducted several exclusions in the dataset. Firstly, we removed individuals who were not enrolled in any insurance scheme, those enrolled in the Urban Employee health insurance program, cases of duplicated insurance enrollment, individuals with commercial health insurance coverage, and participants who were not locally enrolled. We also excluded individuals who were already enrolled in the Urban and Rural Resident Basic health insurance (URRBMI) before 2015. As the primary focus of this study is rural middle-aged and older people individuals, we excluded individuals not residing in rural areas. Finally, we excluded data points where insurance status could not be determined and those with missing variable information. This indicator takes a value of 1 for individuals who experienced the integration of rural and urban resident basic health insurance (URRBMI), and a value of 0 for those who remained under the New Cooperative Medical Scheme (NCMS) coverage.

3.2.3 Control variablesThis study selects control variables from five main aspects:

1. Individual characteristics, including gender (female = 1, male = 0), age, marital status (married or cohabiting = 1, unmarried, divorced, widowed = 0), income (household per capita annual income), years of education (no education or incomplete primary school = 0; primary school = 6; junior high school = 9; high school or vocational school = 12; college degree = 15; bachelor's degree = 16; master's degree = 19; doctorate = 23), number of children (total number of surviving biological and stepchildren), etc. Health behaviors: This encompasses smoking status (smoking = 1; non-smoking = 0), physical exercise (exercise = 1; no exercise = 0), alcohol consumption (drinking = 1; not drinking = 0), and others.

2. Health behaviors: This encompasses smoking status (smoking = 1; non-smoking = 0), physical exercise (exercise = 1; no exercise = 0), and alcohol consumption (drinking = 1; not drinking = 0).

3. Household hygiene environment: The cleanliness of the household is represented by a cleanliness scale (1 = very clean; 2 = quite clean; 3 = clean; 4 = average; 5 = not clean).

4. Quality of medical services and healthcare costs: This is measured by satisfaction with the level of services provided by medical institutions (1 = very satisfied; 2 = satisfied; 3 = neutral; 4 = dissatisfied; 5 = very dissatisfied).

5. Regional fixed effects: Given the varying levels of economic development across different regions, this study controls for regional fixed effects at the provincial level (7, 18, 19). The specific details of each variable can be found in Table 1.

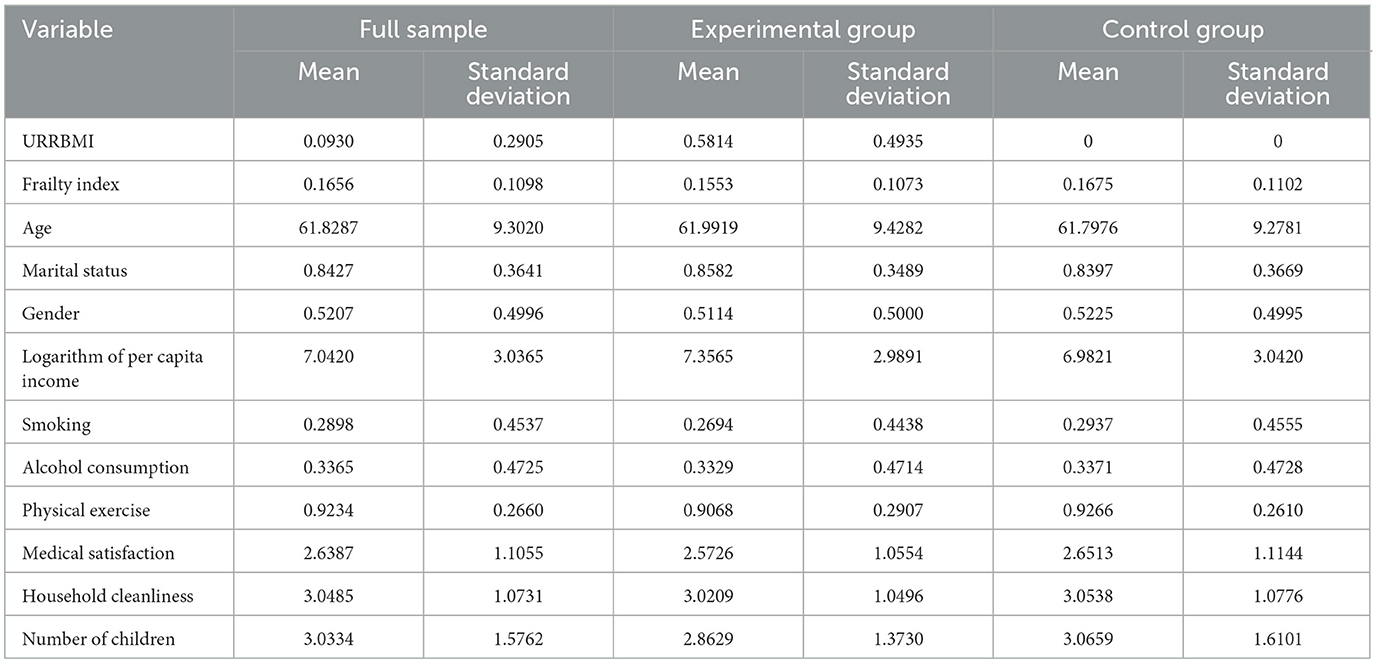

Table 1. Descriptive statistical analysis of the impact of the integration of urban and rural residents' health insurance on health.

3.2.4 Variable descriptive statisticsTable 1 presents the results of the descriptive statistical analysis. In the preliminary examination, it appears that there are not substantial differences between the experimental group and the control group across various variables. Nonetheless, an empirical research analysis is required to assess the impact of the integration of urban and rural residents' health insurance on rural older people individuals.

3.3 Research method 3.3.1 Difference-in-Differences (DID) methodologyBased on the basic steps outlined in the DID model, construct two dummy variables: First, construct dummy variables for the “experimental group” and “control group.” “The experimental group” consists of residents who were covered by the New Rural Cooperative Medical Scheme (NRCMS) in the base year of 2015 and transitioned to the integrated Urban and Rural Residents Basic health insurance (URRBMI) in 2018. The “control group” includes individuals who were covered by NRCMS in both 2015 and 2018. Second, create policy timing dummy variables. By comparing the differences in the health status between the “experimental and control groups,” analyze the impact of the integration of urban and rural residents' health insurance on rural middle-aged and older people individuals. Based on the above analysis, the specific regression model using the Difference-in-Differences (DID) method is as follows:

Yit=β0+β1DIDit+β2Treati+β3Timet+δXit+ϵit (6) DIDit=Treati×Timet (7)Understood. In the model notation, i represents individual or resident, t represents the time period, and Yit represents the health indicator of individual i in time period t.DIDit is the core explanatory variable. Treati is a group dummy variable, where Treati = 1 if i belongs to the experimental group; otherwise, if i belongs to the control group, Treati = 0. Timet is a time-period dummy variable, where Timet=1 if i is in the year 2018; otherwise, if i is not in 2018, ϵit represents the disturbance term. Through the above screening process, a balanced panel dataset was formed with 1,481 observations in the experimental group and 7,774 observations in the control group across two periods.

3.3.2 Quantile Difference-in-Differences (Q-DID)The linear assumptions of the OLS model are likely to mask the effects on older people individuals with different levels of vulnerability. Quantile evaluation methods can comprehensively assess changes in various parameters at different quantile points of the dependent variable (20). Therefore, this study employs the quantile difference-in-differences regression method to investigate the health effects at different quantile points. Setting as follows:

τ(Yit)=β0+β1DIDit+β2Treati+β3Timet+δXit+ϵit (8)τ(Yit) represents the quantile of individual i's health status at time t. The coefficients at different quantiles indicate the impact of urban-rural resident health insurance integration on the health status at that quantile.

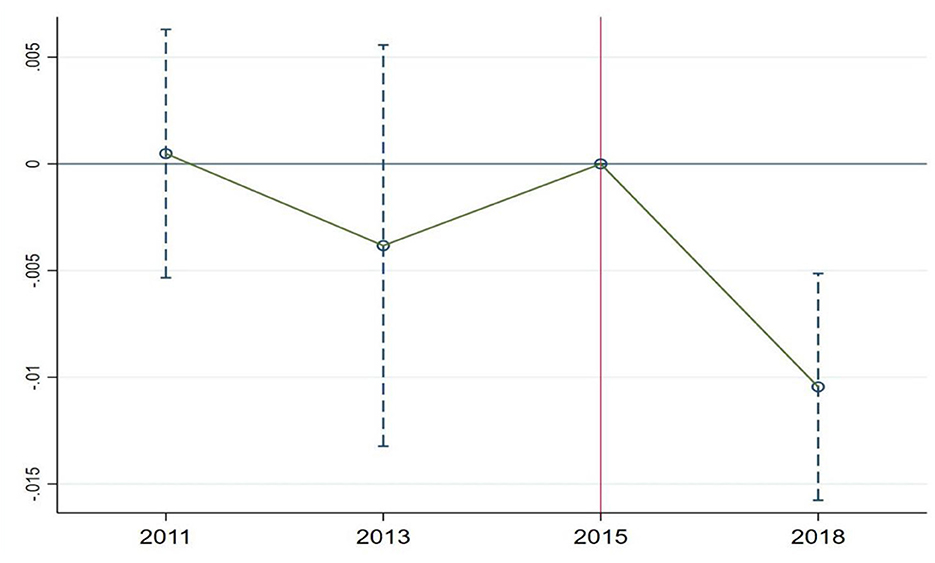

4 Baseline regression analysis of the impact of urban-rural resident health insurance integration on health 4.1 Parallel trends testThe double difference method correctly identifies causal effects under the assumption that the experimental group and the control group have parallel trends before the policy shock. Researchers typically indirectly test the parallel trends assumption by examining whether the pre-treatment trends of the experimental and control groups are the same. This study follows the approach used by Huang et al. to avoid issues of collinearity (21). The base period is set as the year immediately prior to the policy implementation (2015) when the policy took effect (2016). As shown in Figure 3, the coefficients for 2011 and 2013 are not significantly different from 0, indicating that there were no significant differences between the experimental group and the control group in 2011 and 2013 compared to 2015. Therefore, it can be assumed that the pre-treatment parallel trends assumption is satisfied. However, due to the availability of only four waves of CHARLS data, with only three periods before the policy change, it can be challenging to precisely assess parallel trends. To ensure the robustness of the results, this study will further employ robustness analysis methods such as instrumental variable estimation, PSM-DID, and placebo tests in subsequent sections.

Figure 3. Parallel trends test for health.

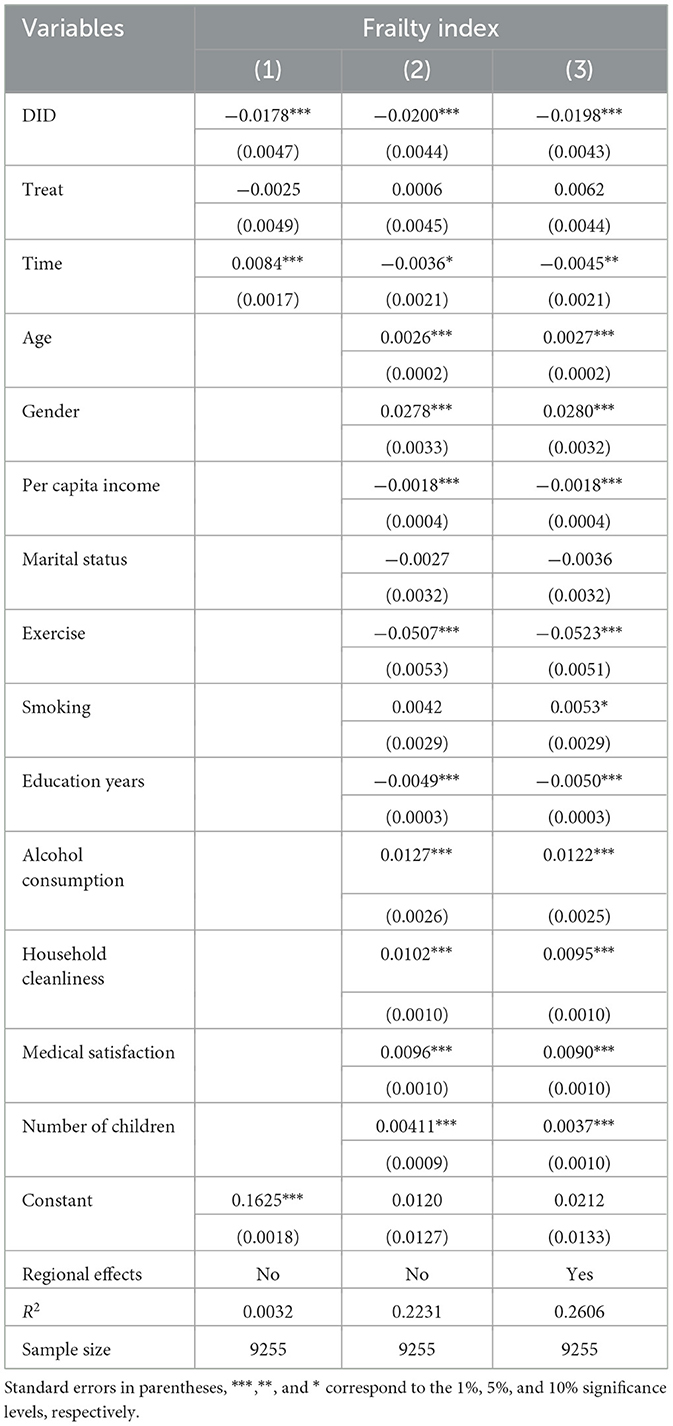

4.2 Baseline regressionAs shown in Table 2, to minimize the impact of omitted variables, Models (1–3) report the regression results under the difference-in-differences (DID) approach without controlling for covariates and province fixed effects, with covariates but without province fixed effects, and with all covariates and regional fixed effects, respectively. Without adding covariates and regional fixed effects, the effect of urban-rural resident health insurance integration on the frailty index is −0.0176. When adding covariates but not province fixed effects, the effect is −0.0200. With all covariates and regional fixed effects included, the effect is −0.0198. The coefficient of the impact remains relatively stable, indicating the robustness of the results. Moreover, whether or not additional control variables and regional fixed effects are included, the effect of urban-rural resident health insurance integration on the frailty index remains statistically significant at the 1% level. Hypothesis 2 has been validated. Although in the short term, the urban-rural resident health insurance integration policy has shown a relatively limited improvement in residents' health, it's important to note that health is a long-term accumulation of capital (1). The impact of urban-rural resident health insurance integration on health is expected to become more significant as time progresses.

Table 2. Baseline regression of the impact of urban-rural resident health insurance integration on health.

In terms of control variables, as individuals age, their physical condition tends to gradually decline, leading to an increase in frailty. Being married, on the other hand, provides more companionship and care. Having a spouse is advantageous for improving health. Income and educational level are directly related to health awareness and health investments. Higher income and educational attainment are associated with better health. Unhealthy habits, such as smoking and alcohol consumption, have a significant negative impact on health, while regular physical exercise can improve health. Improvements in the quality of healthcare services are beneficial for receiving better medical care, which can lead to improved health. Having more children can increase the financial burden on parents, potentially leading to worse health outcomes.

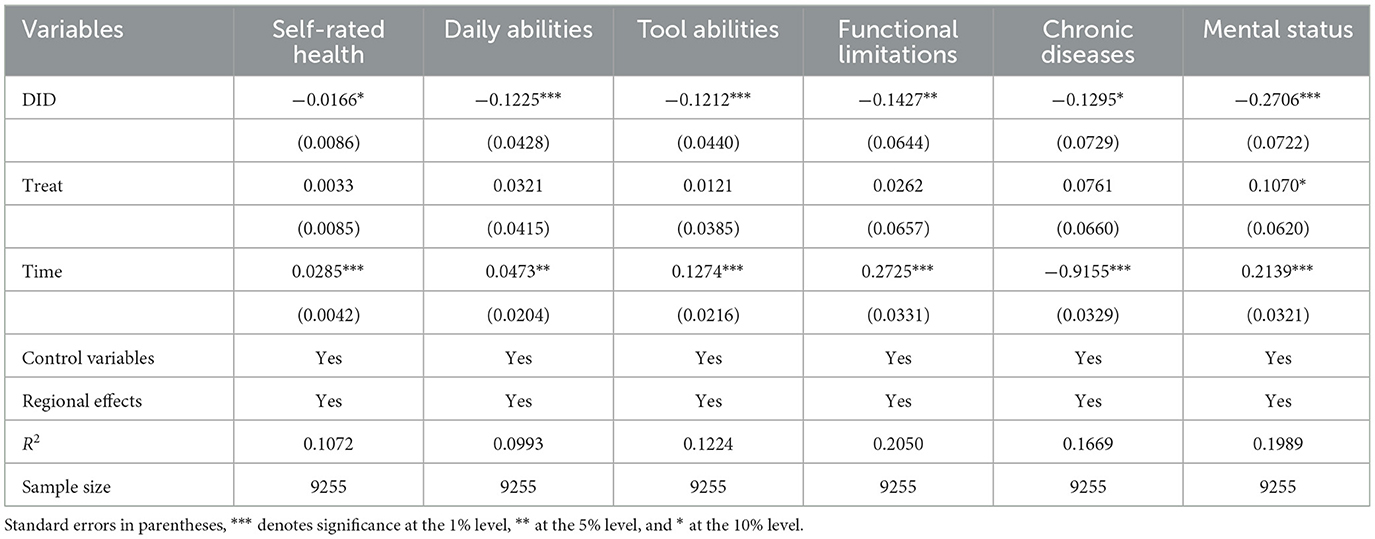

Furthermore, this study conducted regression analyses on different health sub-module indicators. The results showed that whether it's self-rated health, daily activity ability, instrumental activity ability, physical function limitations, chronic disease status, or mental health status, rural older people residents' health significantly improved due to the integration of urban and rural resident health insurance. Among them, self-rated health and mental health are significant at the 1% level, while daily activity ability, instrumental activity ability, and physical function limitations are significant at the 5% level. Chronic disease status is significant at the 10% level (Table 3).

Table 3. Regression analysis of the impact of urban and rural residents' health insurance integration on different health indicators.

On one hand, through regression analysis of different health sub-module indicators, it has been demonstrated that the baseline regression is robust, confirming that the integration of urban and rural residents' health insurance has indeed improved the health status of rural older people individuals. On the other hand, it has also been discovered that the integration of urban and rural residents' health insurance has led to a comprehensive improvement in the health status of rural older people individuals. This improvement is evident in various aspects, including subjective health as reflected in self-rated health, as well as objective physiological health conditions reflected through daily activity capacity, instrumental activity capacity, functional limitations, chronic disease status, and mental health as reflected in psychological and emotional wellbeing. This can be attributed to the fact that the integration of urban and rural residents' health insurance has not only significantly increased the reimbursement rates for medical expenses among rural older people individuals but has also expanded the scope of health insurance coverage and the number of designated hospitals. It has comprehensively safeguarded the healthcare rights and interests of rural older people individuals, leading to significant improvements in the treatment of various diseases and an evident enhancement in their overall health status.

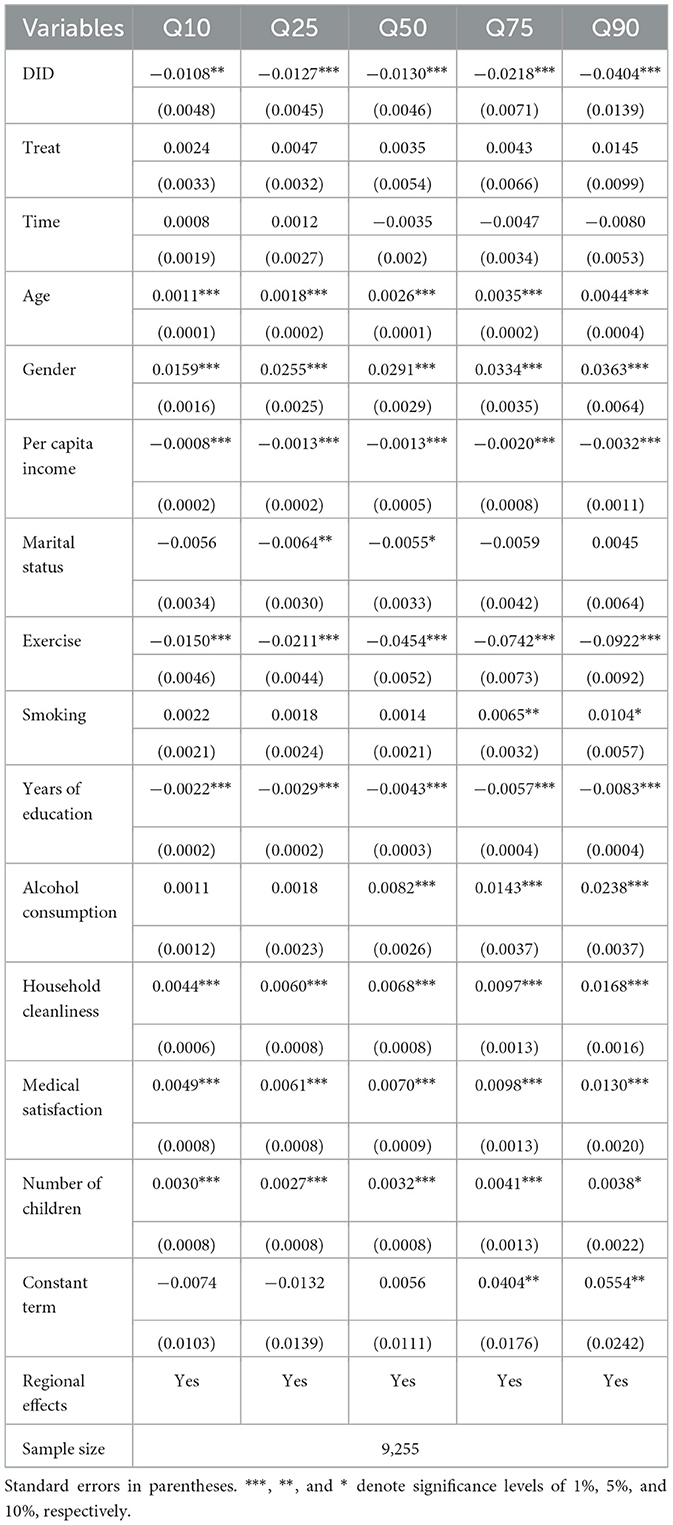

The Chinese basic health insurance system focuses on providing significant coverage for major illnesses, while the coverage for basic diseases is not very high. From this perspective, health insurance is expected to have a greater marginal effect on improving the health of people with serious illnesses, who have lower health levels. In other words, the impact of the integration of urban and rural residents' health insurance on the health of rural older people people should also be non-linear. To test this hypothesis, this study used quantile double-difference regression. The results, as shown in Table 4, reveal that in the quantile double-difference regression, the integration of urban and rural residents' health insurance has a negative impact on the frailty index. Since the frailty index is a negative indicator, this indicates that the integration of urban and rural residents' health insurance significantly improves the health of rural older people individuals. More importantly, this health impact varies significantly at different quantiles of the frailty index.

Table 4. Quantile double difference regression of the impact of urban-rural resident health insurance integration on health.

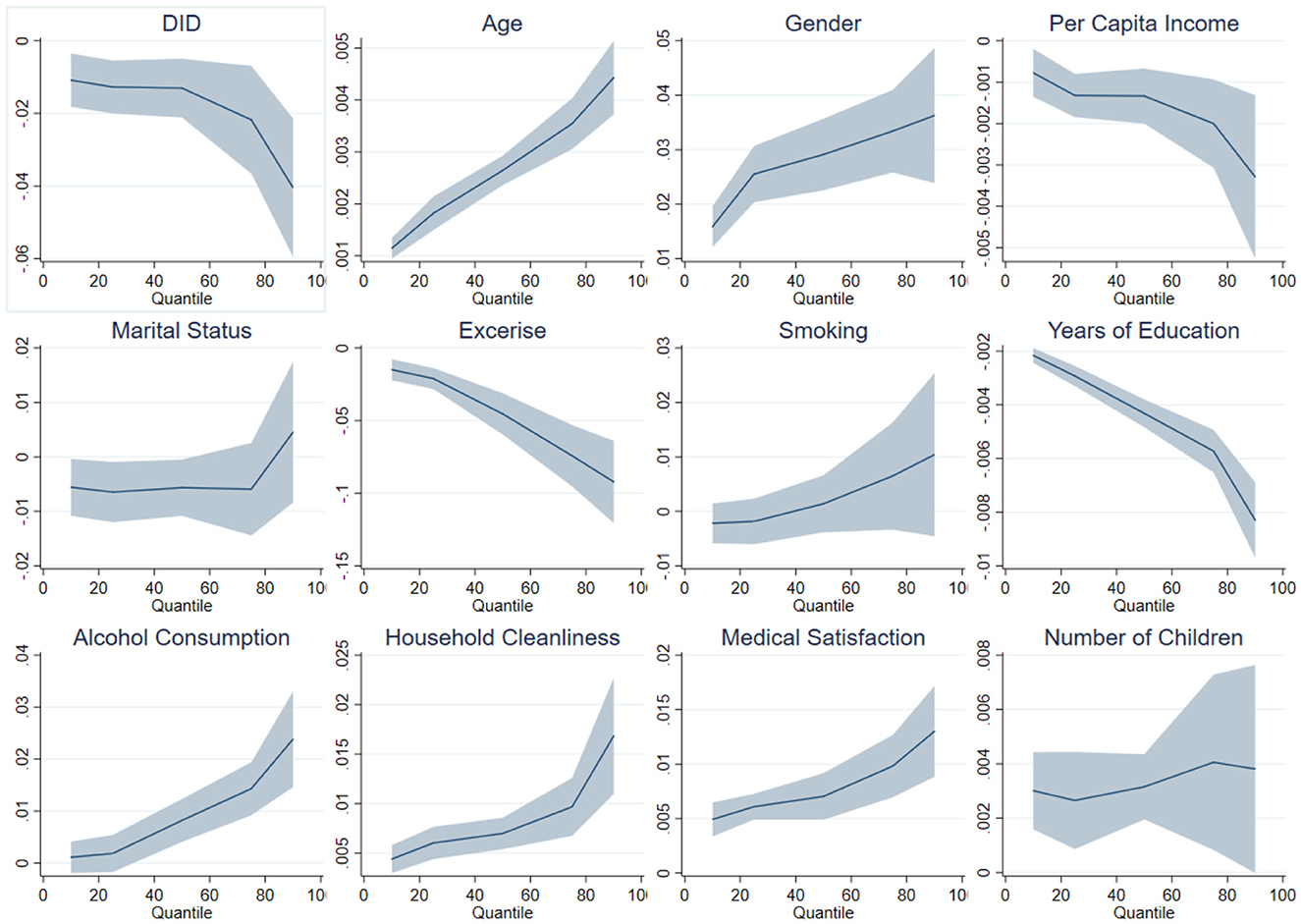

Assuming that the health impact is linear, combined with the previous OLS regression, it is found that the average effect of integrating urban and rural residents' health insurance on the frailty index is a reduction of 0.0198. However, in the quantile double difference regression, at the 10, 25, 50, 75, and 90th percentiles, the integration of urban and rural residents' health insurance led to reductions in the frailty index of 0.0108, 0.0127, 0.0130, 0.0218, and 0.0404, respectively, and these effects were significant at least at the 5% level (Table 4). From the quantile perspective, the impact of the integration of urban and rural residents' health insurance on the frailty index was relatively consistent up to the 50th percentile. However, beyond the 50th percentile, the impact on the frailty index gradually increased, with the most significant effect observed at the 90th percentile, indicating the strongest promotion of health. This study has plotted a trend chart of quantile regression coefficients to provide a more visual representation of this effect (Figure 4).

Figure 4. Quantile coefficient effects of urban and rural resident health insurance integration on health.

4.3 Path analysis of the impact of urban and rural resident health insurance integration on healthHealth insurance can improve residents' health by reducing the financial burden of medical care, increasing the utilization of medical services, and enhancing overall health outcomes. Previous literature has analyzed the pathways through which health insurance affects health, providing valuable insights for the analysis in this study (7, 8, 10, 22–25). This study primarily examines why the integration of urban and rural residents' health insurance has a greater impact on improving the health of rural older people individuals with lower health status. The integration of urban and rural residents' health insurance primarily affects the health status of residents by reducing the financial burden of healthcare. It directly lowers the cost of medical expenses and enhances the utilization of medical services by residents. However, considering the significant amount of missing data in the outpatient and inpatient medical service utilization in the CHARLS dataset, this study, following the approach of Chang et al., chooses healthcare expenditure (annual medical consumption as a proportion of annual total consumption) as a mediating variable in the causal pathway (26). Building on this, the study further investigates the impact of the integration of urban and rural residents' health insurance on the mediating variable, as shown in Table 5. It is evident that the integration of urban and rural residents' health insurance significantly reduces the healthcare expenditure burden on rural older people individuals.

留言 (0)