記住我

Theoretical models that presume human rationality are the mainstream in the field of finance and game research, but in recent years, the rational inattention (RI) model, which explicitly introduces cognitive costs associated with information acquisition and processing, has been attracting attention. The RI model is characterized by the assumption that the cognitive processing cost of information can be measured in terms of the amount of mutual information from the acquired signal. Once this assumption is accepted, theoretically, the existing model can be extended to a more realistic decision-making setting in a relatively natural way, and it also has the great advantage of being able to use the accumulated knowledge in the field of information theory. The RI model has been actively studied as a theory that links decision-making and information theory, and as a modern theory that expresses Simon’s bounded rationality [1–3].

The history of the RI models begins with Sims [4,5], and there have been two major streams of research. The first is the Kalman filter type model initiated by Sims [4]. This model is used in a dynamic environment, in which the accuracy of the filter, or Kalman gain, is determined by the cognitive capacity constraints of information processing. This cognitive capacity, like that in Shannon’s sense, is an upper limit on the total amount of information that can be processed, but in Sims [4] it is determined by the subject’s ability. This model has been applied to many dynamic models, including financial and policy analysis.

Another stream is the stochastic choice type model. This model assumes that information processing costs are incurred in proportion to the amount of mutual information, and given this assumption, people decide not only the action to take but also the amount of information to use to maximize the expected utility. This model is known to be closely related to logit-type stochastic choice models [6] and has been applied to a variety of fields including game theory. Over recent years, there has been progress in the refinement of information cost modeling and in extending it to dynamic environments.

However, in contrast to this energetic promotion of the theoretical works, empirical verification of the validity of the RI model has not progressed much. There have been only a few behavioral experiments and even fewer in more realistic settings. Furthermore, to our knowledge, the central assumption of the RI model, that the amount of mutual information obtained from signals adequately represents the cognitive cost of information, has not been tested from a neuroscientific perspective. The present study aims to test this point.

A central assumption of the RI model is that it assumes cognitive costs concerning people’s information processing. In this paper, we conducted two types of experiments, one with and one without exogenous control of the information given, and examine the correspondence between the model parameters related to cognitive costs estimated from the participants’ choices and their brain responses. Specifically, we will examine whether the cognitive processing cost of the model is consistent with the activation of brain regions related to working memory and reasoning, such as the dorsolateral prefrontal cortex, ventral prefrontal cortex, and rostral prefrontal cortex. The analysis was conducted using both the stochastic choice type and the Kalman filter type models, but due to space limitations, the present text refers only to the stochastic choice type, which better explained the behavior of the experimental participants. Comparison with the Kalman filter type is made in Supplemental Materials C, Supplemental Digital Content 1, https://links.lww.com/WNR/A675.

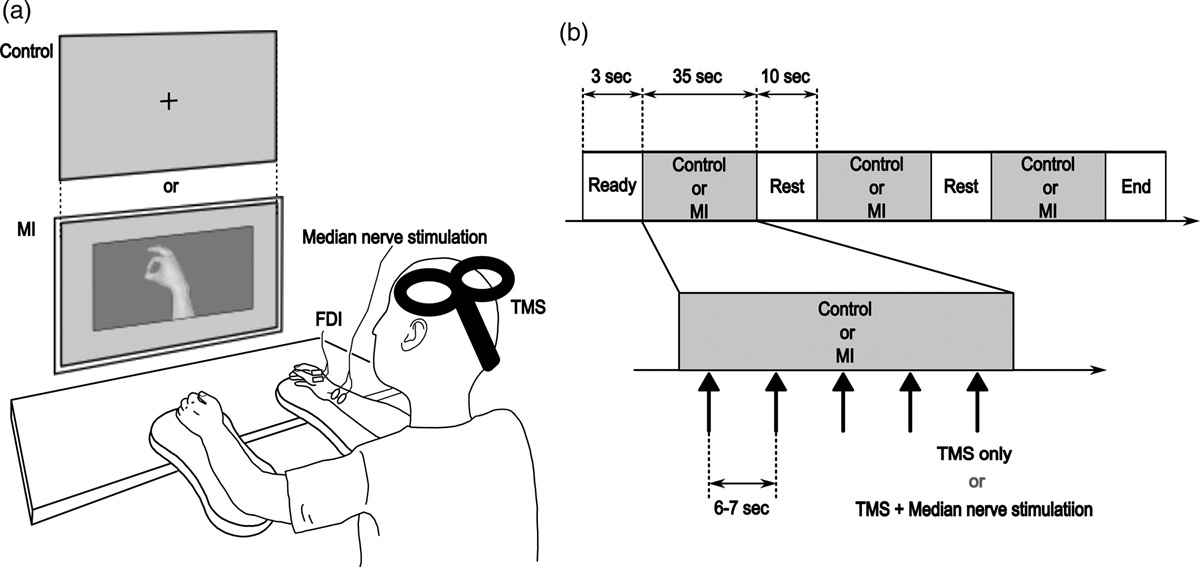

Experiment 1 Experimental setupThis experiment was conducted under the approval of the Ethics Committee of the Tokyo University of Science. The participants of this experiment were 10 undergraduate and graduate students (40 samples) of the School of Business, Tokyo University of Science. We explained the details to all participants in advance of the experiment and obtained their written consent.

We use the sequential investment task with a view to the application [7,8]. In this task, participants make predictions about the return of a price sequence each period and decide whether to invest in a single stock or a safe asset. The participant’s goal is to maximize the expected return. The fundamental return of the stock, denoted by f, is randomly set at the beginning of each price sequence and is constant over time. The return observed in each period t is defined by rt=f+εt, where εt∼N(0,σN2)i.i.d. represents shocks other than fundamental, such as market factors. The return on the safe asset is always assumed to be rS=0. The price sequence presented to the participant’s graphical user interface (GUI) is calculated as Pt+1=(1+rt)Pt. Therefore, when the fundamental return is zero, f=0, the price will randomly walk.

The participant can predict the fundamental return f from the observed returns. If there is no cognitive constraint on information processing, fundamental returns f can be identified from the law of large numbers by using a large enough number of past returns and taking the average of the time series. However, if there is a cognitive constraint, participants may not reasonably formulate a prediction because it takes a certain amount of calculation to obtain each period’s returns from prices and to take their average (RI).

The left panel of Fig. 1 shows the experimental GUI that participants faced during the decision-making process. To avoid biometric artifacts caused by the button selection behavior, the experiment used a cylinder-type input to allow the investment rate to be varied continuously. For more information on the sequential investment task, please see Supplemental Materials A, Supplemental Digital Content 1, https://links.lww.com/WNR/A675.

Fig. 1:

Fig. 1: The left figure is experimental setup the right figure is brain regions of interest.

The biometric information used in this analysis was the change in blood hemoglobin concentration in the prefrontal area. Functional NIRS (BriteMKII supplied by Artinis Medical Systems, Tokyo, Japan) was used to measure the blood hemoglobin concentration in the prefrontal area. The right panel of Fig. 1 shows the brain regions that we focused on in this study. We will focus on the dorsolateral, ventral, and rostral regions, which are considered to be closely related to costly cognition, working memory, and reasoning. The prefrontal cortex may be roughly divided into the orbitofrontal cortex , medial prefrontal cortex (BA 24, 25, 32, and mesial portions of 10), and dorsolateral cortex (BA 8, 9, and 46). Each region has a distinct cytoarchitecture and function as well as distinct connections. Briefly, the orbitofrontal cortex is involved in decision-making, processing awards, and punishment; and the medial prefrontal cortex, particularly the anterior cingulate cortex, mediates emotional monitoring, and self-regulation. The dorsolateral prefrontal cortex (including BAs 46, 9) is involved in working memory. Working memory is the ability to hold a limited amount of information in mind for a short period. For example, working memory is necessary for holding a phone number ‘in mind,’ or keeping track of geographical locations as someone gives you multistep directions to a location across town. This type of memory is critical to bridging temporal gaps so that the information can be ‘worked’ with or mentally manipulated for a short period. This ability to hold representations in mind is critical to other complex cognitive functions, such as decision-making, planning, and problem-solving. Area 8A can be considered as a key area for the top-down control of attentional selection, it is also a very important region for this experiment, but this time we used NIRS as experimental equipment, so it was difficult to measure Area 8A [9–15]). Table 1 shows the regions of interest and the corresponding Montreal Neurological Institute coordinates.

Table 1 - MNI coordinates Region of interest Brodmann areas MNI coordinates of the center of gravity x y z CH19 Brodmann area 10 23 55 7 CH21 Brodmann area 9 −39 34 37 CH22 Brodmann area 46 −46 38 8MNI, montreal neurological institute.

We focus here only on the results of the stochastic choice RI model, see Supplemental Materials C, Supplemental Digital Content 1, https://links.lww.com/WNR/A675, for details on the analysis and mosdel comparison in the Kalman Filter RI model. In the stochastic choice type RI model, people are assumed to decide on two steps [6]. The first step is to choose the information strategy to use, and the second step is to choose the action to optimize the expected profit based on the prediction/belief of the fundamental return. It is optimal to use as many and as useful signals as possible to identify the fundamental returns, but a certain percentage of cognitive cost λ is required in proportion to the amount of mutual information obtained from the signals.

More specifically, in the second stage, people decide whether to invest in the stock or safe asset according to the conditional distribution of the fundamental return P(f|s) given signals, denoted by s. The observed past returns in experiment 1 and the associated stock returns in experiment 2 serve as signals, respectively. The utility realized with an optimal action at this stage is denoted by V(p(f|s)). In the first stage of information strategy selection, given the expected utility, people decide which signals to use. The choice of information strategy determines which signal structure p(s,f) is desirable. To obtain more detailed information, a cost λ is incurred according to the amount of mutual information, where H is the Shannon entropy, and the amount of mutual information is defined as the decrease in entropy due to the acquisition of the signal. λ is a parameter that represents the cognitive cost per unit of mutual information. The first-stage problem can be written as follows:

maxp(s|f)∑f∑sV(p(f|s))p(s|f)p(f)−λ,

where we assume that the possible states of the fundamental return are finite to keep the discussion simple.

Assuming that the ex-ante choice probabilities of a stock and safe asset are equal before the fundamental returns are given in the experiment (the expected value of the fundamental return f given in this experiment is zero, which is equal to the return of the safe asset), the solution to this problem can be derived by the following SoftMax-type choice rule1.

pt=exp(fλ)/,∀t

If the cost is infinite, pt=12 the subject will be a person who chooses completely randomly. On the other hand, when a hyper-rational person with no information cost, he will gather information and choose the option with the lower payoff with probability 0, or the option with the higher payoff with probability 1.

The model parameter λ was estimated using maximum likelihood estimation from the observed investment choices of participants and the given values of the fundamental return f. Please refer to Supplemental Materials A and B, Supplemental Digital Content 1, https://links.lww.com/WNR/A675, for details of the estimation.

Results of experiment 1 Quantile analysisFirst, we will refer to the relationship between the variance of investment rate and blood hemoglobin concentration. The scatter plot of the relationship in Supplemental Materials D, Supplemental Digital Content 1, https://links.lww.com/WNR/A675, shows that a positive correlation between the investment variance and the hemoglobin concentration in the brain area can be observed. From the above equation, the larger the information processing cost λ, the closer the investment probability P is to 1/2, and the larger the investment variance. This result indicates that brain regions related to information processing and cognition are activated when the variance of the investment rate is large, which is consistent with the predictions by the RI model.

Next, we will examine the relationship between the estimated parameter values of each RI model and the hemoglobin concentration in the blood. As mentioned earlier, the amount of mutual information obtained from signals is determined subjectively, and this cannot be observed directly. The parameters of each model can be considered as its alternative indicators. Figure 2 shows the average hemoglobin concentration in the blood of each group in dichotomous analysis, and Fig. 3 shows the average hemoglobin concentration in the blood of each group in the trichotomous analysis. The figure on the left shows the hemoglobin concentration in the blood of each sample, divided into two or three groups according to the size of the estimated model parameter λ (the left bar shows a small value group and the right bar is a large value group). From left to right, they correspond to rostral, dorsolateral, and ventral lateral regions. The right of Fig. 2 is a scatter plot of the parameter for each sample and the blood hemoglobin concentration in the extraperitoneal region.

Fig. 2:

Fig. 2: Correlation with λ, dichotomous analysis.

Fig. 3:

Fig. 3: Trichotomous analysis of λ.

From these figures, we can see that brain activity is consistent with the assumptions of the RI model. In other words, the larger the cognitive cost λ the more activated the brain regions involved in costly cognition. The differences between these groups are significant for λ in all brain regions in the dichotomous partition and all brain regions except the rostral region in the tripartite partition (5% level in the F-test of ANOVA analysis).

Model selectionFinally, we examined a more appropriate model based on the behavioral data, using the maximum likelihood method for model fitting. Table 3 in Supplemental Materials C, Supplemental Digital Content 1, https://links.lww.com/WNR/A675, summarizes the log-likelihood (llh), Akaike’s information criterion, and R2 (R2) for the stochastic choice type RI models. R2 is the improvement in the llh from a random prediction, defined as follows, R2=logM−logMrand−logMrand, where M is the likelihood of the model concerned, and Mrand is that of the random prediction model.

The table clearly shows that the stochastic choice type is superior for this experimental data (please refer to Supplemental Materials C, Supplemental Digital Content 1, https://links.lww.com/WNR/A675, for definitions of six variants of the Kalman filter type RI models). As for the change in blood hemoglobin concentration, the correlation between the parameters of the stochastic choice type model was clearer than that of the Kalman filter type model, and the same tendency was observed for the behavioral data.

Experiment 2To further clarify the causal relationship between the amount of information processed and its cognitive cost, we also conducted an experiment in which we controlled for the amount of information available. Here, we focused on the RI model of the stochastic choice type that is most appropriate for the analysis in Section ‘Quantile analysis’. Figure 4 shows the PC screen presented to the experimental participants in experiment 2. In this experiment, participants are presented with a series of prices of stocks to be invested in (say the target stock price, which is shown at the center of the screen) and a series of prices of stocks that have some correlation with that stock price (left two columns of the screen, signal stock prices). Participants can predict the target stock price to invest in from these signal stock price columns, and based on this prediction, they choose whether to invest in the target stock price or held it in a safe asset.

Fig. 4:

Fig. 4: GUI image. GUI, graphical user interface.

In this experiment, three treatments were conducted: treatment 1 is a control condition and only one signal stock price is presented; in treatment 2 and treatment 3, the number of signal stock prices presented is increased to 4 and 8, respectively. The more stock prices that are signals, the more information is available, and more accurate predictions of the target stock price can be made, but on the other hand, there is more information needed to process, resulting in cognitive costs and inattention. In the experiment, target and signal stock price sequences for 30 periods are initially presented, followed by investment choices for 170 periods.

As in experiment 1, brain blood hemoglobin concentration was measured during decision-making. The measurement sites are the same as in experiment 1 shown in Table 1. The participants in the experiment were 21 undergraduate and graduate students at the Tokyo University of Science. The number of valid samples was 42, each sample corresponding to one treatment. As in experiment 1, participants were paid for their performance. See Supplemental Materials B, Supplemental Digital Content 1, https://links.lww.com/WNR/A675, for details on the experimental setup and model.

Figure 5 in Supplemental Materials D, Supplemental Digital Content 1, https://links.lww.com/WNR/A675, shows the sample mean of the information cost calculated from the model for each treatment. As intended, we see that the information cost increases as the number of signals controlled for increases, and the sample means per treatment starting from treatment 1 are, 172.97, 1523.59, and 2124.09. As in Section ‘Stochastic choice type rational inattention model’, the calculation of the information cost is given by λ multiplying the amount of mutual information obtained from the signals by the cost parameter, and the ANOVA analysis shows a significant difference for each treatment group (F value = 3.48; P = 0.0405).

Next, we examined how blood hemoglobin concentrations in brain regions differed from treatment to treatment. If the cognitive information processing cost modeling by RI is appropriate, we should be able to observe the activation of the regions that are supposed to be responsible for information processing in proportion to the amount of information controlled for and the information cost. Figure 5 is the sample mean of the OxyHb change (170 periods) in the dorsolateral region for each treatment. The ANOVA analysis shows a significant difference from the control group (F value = 2.87; P = 0.0685; left panel: F value = 2.94, P = 0.0649; right panel: F value = 2.94; P = 0.0649). The tendency is more pronounced in treatment 3 with eight signals are presented, which are expected to have exceeded the cognitive capacity. On the other hand, in treatment 2, which has four signals, information is processed relatively stress-free, as in treatment 1, which has one signal.

Fig. 5:

Fig. 5: Relationship between each treatment and OxyHb concentration. The horizontal axis is treatments 1, 2, and 3 from left to right, and the vertical axis is the normalized blood OxyHb concentration increase averaged over all samples. The left figure shows BA46 and the right figure shows BA9.

DiscussionSo far, the number of empirical studies on the RI models is not large. Deany and Nelighz [16] have a ball task and Dewan and Neligh [17] use a uniform guess task to examine the validity of information cost representations by Shannon entropy and Tsallis entropy. However, these studies do not directly test the central assumptions of the RI model, specifically the validity of expressing cognitive processing costs in terms of the mutual information content of information, from a neuroscientific perspective. In this paper, we have examined the correspondence between the amount of mutual information and cognitive cost from a biometric perspective. Our analysis showed that the cost parameter λ of the stochastic choice type model was significantly positively correlated with the activation status of the rostral prefrontal cortex and dorsolateral prefrontal cortex. These brain regions are known to associate with costly cognition and be activated during information integration and working memory utilization. This result suggests that the cognitive cost represented by the amount of mutual information employed in the RI model is consistent with the activation of brain regions associated with cognitive cost, and, thus, indirectly supports the assumption of the RI model.

Acknowledgements Conflicts of interestThere are no conflicts of interest.

References 1. Simon HA. A behavioral model of rational choice. Q J Econ. 1955; 69:99–118. 2. Simon HA, Barenfeld M. Information-processing analysis of perceptual processes in problem solving. Psychol Rev. 1969; 76:473–483. 3. Mackowiak B, Matejka F, Wiederholt M. Rational inattention: a review. CEPR Discussion Papers; 2020:15408. 4. Christopher A. Sims: implications of rational inattention. J Monet Econ. 2003; 50:665–690. 5. Christopher A. Sims: rational inattention: beyond the linear-quadratic case. Am Econ Rev. 2006; 96:158–163. 6. Matejka F, McKay A. Rational inattention to discrete choices: a new foundation for the multinomial logit model. Am Econ Rev. 2015; 105:272–298. 7. Shimokawa T, Suzuki K, Misawa T, Miyagawa K. Predictability of investment behavior from brain information measured by functional near-infrared spectroscopy: a bayesian neural network model. Neuroscience. 2009; 161:347–358. 8. Shimokawa T, Kinoshita K, Miyagawa K, Misawa T. A brain information-aided intelligent investment system. Decis Support Syst. 2012; 54:336–344. 9. Matejka F. Rigid pricing and rationally inattentive consumer. J Econ Theory. 2015; 158,656–678. 10. D’Esposito M, Detre JA, Alsop DC, Shin RK, Atlas S, Grossman M. The neural basis of the central executive system of working memory. Nature. 1995; 378:279–281. 11. Smith EE, Jonides J. Neuroimaging analyses of human working memory. Proc Natl Acad Sci U S A. 1998; 95:12061–12068. 12. Smith EE, Jonides J. Working memory: a view from neuroimaging. Cogn Psychol. 1997; 33:5–42. 13. Gupta R, Tranel D. Memory, neural substrates. Encyclopedia of human behavior; Elsevier Inc. 2012:593–600. 14. Germann J, Petrides M. Area 8A within the posterior middle frontal gyrus underlies cognitive selection between competing visual targets. eNeuro. 2020;7:ENEURO.0102–ENEU20.2020. 15. Hamid H. Networks in mood and anxiety disorders. Neuronal networks in brain function, CNS disorders, and therapeutics; Elsevier Inc. 2014:327–334. 16. Deanyand M, Nelighz N: Experimental tests of rational inattention. Columbia University Libraries. 2017. doi: 10.7916/d8-4w4k-3q85 17. Dewan A, Neligh N. Estimating information cost functions in models of rational inattention. J Econ Theory. 2020; 187:105011.

留言 (0)