記住我

Older adults are at elevated risk for being diagnosed with neurodegenerative conditions such as Alzheimer's disease (AD), and some studies suggest brain changes may occur at least 20 years prior to the onset of the clinical symptoms (Alzheimer's Disease Facts and Figures, 2020). Data projections indicate a 22% increase in the number of AD cases from about 5.8 million in 2020 to about 7.1 million in 2025 (Alzheimer's Disease Facts and Figures, 2020). Older adults, who hold about 70% of all disposable income, are vulnerable to making suboptimal financial decisions such as choosing poor investments (Gamble, Boyle, Yu, & Bennett, 2015; Korniotis & Kumar, 2011). A recent large-scale population-based study found that delinquent credit card payments and subprime credit scores were present in Medicare beneficiaries about 6 and 2.5 years prior to a dementia diagnosis, respectively (Nicholas, Langa, Bynum, & Hsu, 2021). Older adults are also highly prone to financial exploitation, with data suggesting a related net loss of $2.9 billion to $36.5 billion (Consumer Financial Protection Bureau, 2017). These observations necessitate a thorough investigation of financial decision-making (FDM) and its constituent elements in the context of various brain-related indices in healthy older adults.

FDM is a multidimensional construct, and is generally defined as the ability to autonomously conduct financial tasks in order to manage one's finances without error or preventable financial loss (Lichtenberg, Ficker, & Rahman-Filipiak, 2016; D. C. Marson et al., 2000). There are important differences in the concepts of financial ability, capability, competency, or capacity. For example, the term financial competency is used in forensic settings, while the term financial capacity is used in the context of medical/clinical evaluations. However, these terms are sometimes used interchangeably, even though they are not synonymous (Lichtenberg, Stoltman, Ficker, Iris, & Mast, 2015; D. Marson, 2016; National Academies of Sciences, Engineering,, & Medicine, 2016). Older adults are vulnerable to making suboptimal financial decisions such as displaying substandard credit card behaviors, and annual financial losses are estimated to range from $2.9 billion to $36.5 billion (Acierno et al., 2010; Agarwal, Driscoll, Gabaix, & Laibson, 2009; Conrad, Iris, Ridings, Langley, & Wilber, 2010; Consumer Financial Protection Bureau, 2017).

Financial awareness is a critical, but often overlooked, aspect of FDM that is distinct from FDM itself. For example, while everyday FDM typically involves activities such as paying bills, purchasing goods, and saving money, financial awareness is the extent to which an individual accurately perceives his or her own FDM skills. Financial awareness, analogous to FDM, can be construed as a multifaceted construct. One facet, “offline” (e.g., global, day to day) awareness of one's current, personal financial circumstances, can be challenging to assess without direct knowledge of the individual's actual circumstances (e.g., credit score, history of vulnerability to scam, etc.), and informants are not always accurate in their impressions of an individual's circumstances or abilities (Martyr & Clare, 2018; Sunderaraman, Cosentino, Lindgren, James, & Schultheis, 2018). Another facet of financial awareness relates to “online,” or in the moment, awareness of performance on a financial task (Sunderaraman, Chapman, Barker, & Cosentino, 2020). Several studies have shown that metacognitive tasks which measure online awareness of abilities such as memory and executive function relate to more global levels of awareness for these abilities in day-to-day life (Cosentino, Metcalfe, Butterfield, & Stern, 2007; Cosentino, Metcalfe, Cary, De Leon, & Karlawish, 2011; Koren et al., 2004).

Relative to studying structural brain regions via volume and cortical thickness in older adults, examining white matter integrity offers another perspective on how the aging brain may be linked to FDM. White matter, consisting of myelinated axons and glia, is responsible for communication among different brain regions. White matter integrity as measured by diffusion tensor imaging (DTI) examines the cohesion of axonal tracts by detecting the diffusion of water molecules. In intact axons relative to damaged ones, the diffusion of water is more anisotropic which reflects as higher fractional anisotropy (FA) and lower diffusivity (Mori & Zhang, 2006). Studies report that compared to measures of structural integrity such as cortical thickness, white matter integrity is more closely associated with cognitive aging (Ziegler et al., 2010). Therefore, it becomes important to examine whether and how white matter is associated with FDM and financial awareness.

In healthy older adults, FDM is strongly associated with numerical and reasoning abilities (Boyle et al., 2013; Demakis, Szczepkowski, & Johnson, 2018; Sunderaraman, Barker, Chapman, & Cosentino, 2020), and studies have linked numerical/arithmetic abilities to specific white matter networks (Grotheer, Zhen, & Grill-Spector, 2019). For example, the superior longitudinal fasciculus (SLF) along with the arcuate fasciculus (AF) are implicated in numerical/mathematical abilities such as adding in some studies, while other studies identified tracts including corticospinal tract (CST), cingulum-cingulate gyrus (CCG), and the inferior longitudinal fasciculus (ILF) (Grotheer et al., 2019; Matejko & Ansari, 2015; Moeller, Willmes, & Klein, 2015). In another study, temporal discounting, the tendency to prefer smaller monetary rewards over a shorter time period compared to larger rewards over a longer time period, was associated with reduced integrity of the bilateral frontal, frontostriatal, and temporal–parietal white matter tracts (Han et al., 2018). Across most studies, the SLF has been recognized consistently as an important tract for numeracy, making it a prime candidate for supporting healthy FDM in older adults (Matejko & Ansari, 2015).

While studies, although quite limited, have examined the links between white matter and FDM, the association of white matter integrity in relation to awareness of one's FDM (i.e., financial awareness) has yet to be examined. FDM and financial awareness, both measured using standardized, objective tools, involve different neuroanatomical substrates. Cortical thickness, while not associated with everyday FDM in cognitively healthy older adults, was associated with financial awareness (Sunderaraman et al., 2021). Specifically, thinner right temporal cortex (temporal pole, parahippocampus, and entorhinal regions) was linked to overconfidence in one's financial abilities. Relatedly, other studies found that right temporal compromise is involved in increased risk for scam susceptibility and financial exploitation (Han et al., 2016; Lamar et al., 2020; Spreng et al., 2017). Specifically, lower white matter integrity in the right temporal–parietal and temporal–occipital regions was associated with increased self-reported scam susceptibility in a sample of older adults without dementia (Lamar et al., 2020). Overall, studies of self-awareness have found greater involvement of right versus left neural substrates and connections. We therefore expected the right-lateralized networks to be most strongly related to financial awareness. Borrowing from the broader self-awareness literature, there is also emerging evidence that the SLF tracts are associated with other aspects of self-referential processing involving motor awareness (Pacella et al., 2019). Therefore, we anticipated that the SLF tracts connecting the frontal–temporal–parietal regions would also be implicated in financial awareness, perhaps with a differential role for right-sided tracts.

Different types of white matter metrics can contribute to different task-tract associations. For example, FDM was associated with FA, but not diffusivity, in the cingulo–parietal–frontal and temporo-occipital regions in those with mild cognitive impairment (Gerstenecker, Hoagey, Marson, & Kennedy, 2017). In the same study, mean diffusivity (MD), but not FA, in the anterior cingulate, callosum, and frontal regions, were associated with FDM in those with AD (Gerstenecker et al., 2017). Therefore, in the current study, we examined the association between financial awareness and white matter integrity using FA and MD metrics.

A few different methods are available for processing diffusion images, including voxel-based spatial statistics (TBSS) (Soares, Marques, Alves, & Sousa, 2013) and TRActs Constrained by UnderLying Anatomy (TRACULA). While TRACULA is an automated probabilistic tractography toolbox within Freesurfer (Yendiki et al. (2011a, 2011b)), voxel-based methods require accurate registration algorithms using tensor datasets (Mukherjee, Chung, Berman, Hess, & Henry, 2008). Compared to voxel-based approaches, tract-based approaches, such as TRACULA, may be less able to detect abnormalities in the tracts if these are not universally present throughout the given tract. On the other hand, TRACULA is less fraught by inaccuracies associated with intersubject registration given that quantification automatically occurs within an individual subject's space (Mak et al., 2021; Mamah, Ji, Rutlin, & Shimony, 2019).

To summarize, the current study examined the associations of white matter integrity using TRACULA with FDM and financial awareness. We hypothesized that measures reflecting white matter integrity in the SLF connecting the temporal and frontal regions would be most strongly associated with both FDM and financial awareness. Based on previous studies, we did not expect FDM to be lateralized, and therefore investigated 8 bilateral white matter tracts in addition to forceps minor, forceps major, and the across tract average. In the case of financial awareness, right-sided SLF tracts were hypothesized to be the most salient fibers. An exploratory aim was to examine the association of integrity measures derived in all 18 white matter tracts with FDM and financial awareness.

2 MATERIALS AND METHODS 2.1 ParticipantsParticipants were recruited for the Reference Ability Neural Network (RANN) Study (Stern et al., 2014), wherein neuroimaging data were collected. Data for the current study were then prospectively collected from 60 cognitively healthy older adults in a single session examining FDM, financial awareness, and memory awareness (average months between RANN participation and current study = 7.8 months). Participants were required to be native English speakers, strongly right-handed (determined via a set of items administered during the telephone screen), and have a minimum of fourth-grade reading level (Stern et al., 2014). They were screened for dementia or MCI using the Dementia Rating Scale with a minimum cutoff score of 130 (Mattis, 1988), hearing and/or visual impairment, and MRI contraindications. Written informed consent was obtained from all participants and compensation was provided at the end of the study. The Columbia University Medical Center Institutional Review Board approved this study.

2.2 Financial decision-makingTwenty objective items from the Financial Competence Assessment Inventory were used (Kershaw & Webber, 2008; Sunderaraman et al., 2018; Sunderaraman, Chapman, et al., 2020). Items were either performance-based and observable (e.g., writing a check) or were conceptual knowledge questions that could be scored objectively with an external criterion (e.g., what is the meaning of assets?). Examples of other items include ability to: understand bills, fill out an insurance form, and perform basic arithmetic calculations based on a hypothetical situation. Accuracy was originally scored on a scale from 1 to 5, but was collapsed into 1 to 3 because of the distribution of the data (Sunderaraman, Chapman, et al., 2020). The total accuracy ranged from 20 to 60.

2.3 Financial awarenessBefore and after each Financial Competence Assessment Inventory item, participants made prospective and retrospective judgments about their performance (How confident are you that you answered that question correctly?) on the specified item on a scale from 1 (unsure) to 4 (very confident). Because of the high correlation between the judgments (Sunderaraman, Chapman, et al., 2020), only prospective judgments were used in this study. The 4-point scale was collapsed into a 3-point scale ranging from 1 to 3 to bring it numerically on the same scale as the FCAI accuracy ranges. This matching enabled calculation of the awareness score; details regarding the development of the confidence rating scale can be found in Sunderaraman, Chapman, et al. (2020). Based on established metacognitive frameworks (Cosentino et al., 2007; Dunlosky & Tauber, 2016), calculation of calibration required that the average accuracy on the FDM task be subtracted from the average prediction score (i.e., individuals' confidence ratings predicting how they would perform) to determine the extent to which individuals were overconfident or underconfident. A score of zero indicated perfect calibration, positive scores indicated overconfidence, and negative scores indicated under confidence in one's financial abilities (total score range: −2 to 2).

2.4 Procedures 2.4.1 MRI acquisitionMRI images were acquired in a 3.0 T Philips Achieva scanner using a standard quadrature head coil. A T1-weighted scout image was acquired to determine subject position followed by a T1-weighted MPRAGE scan with a TE/TR of 3/6.5 ms and flip angle of 8°, in-plane resolution of 256 × 256, field of view of 25.4 × 25.4 cm, and 165–180 slices in axial direction with slice-thickness/gap of 1/0 mm. The DTI images were acquired in 55 directions with 1 b-0 volume using these parameters: b = 800 s/mm2; TE = 69 ms; TR = 11,032 ms; flip angle = 90°; in-plane resolution 112 × 112 voxels; acquisition time 12 min 56 s; slice thickness = 2 mm (no gap); and 75 slices.

Any T1-weighted scans with potentially clinically significant findings were reviewed by a neuroradiologist and removed from the sample prior to the current analysis. However, no clinically significant findings were identified or removed.

2.5 Structural T1 processingSegmentation of the T1-weighted image was a necessary step in processing the DTI data. Each subject's structural T1-weighted scan was reconstructed using FreeSurfer v5.1 (http://surfer.nmr.mgh.harvard.edu/). Each subject's white and gray matter boundaries as well as gray matter and cerebral spinal fluid boundaries were visually inspected slice by slice, manual control points were added in the case of any visible discrepancy, and reconstruction was repeated until we reached satisfactory results within every subject based on visual inspection. The subcortical structure borders were plotted by FreeView visualization tools and compared against the actual brain regions. In case of discrepancy, they were corrected manually.

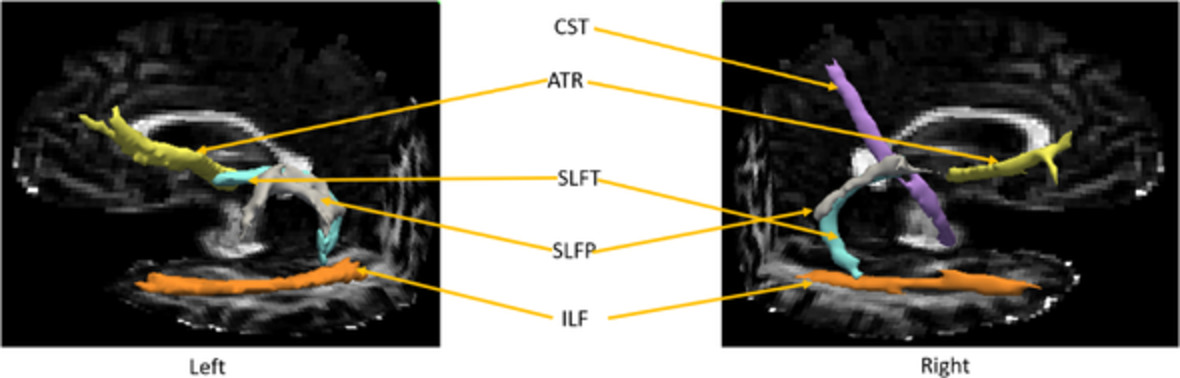

2.6 DTI analysis DTI data were processed with TRACULA distributed as part of the FreeSurfer v. 5.2 library (Yendiki et al. (2011a, 2011b)). This older version of the software was used to ensure consistency across the entire study cohort. The software produces 18 major white matter tracts, along with the overall tract average, as listed below: forceps major, which passes through genu of corpus callosum (FMAJ); forceps minor, which passes through splenium of corpus callosum (FMIN); bilateral anterior thalamic radiation (ATR); bilateral cingulum - angular (infracallosal) bundle (CAB); bilateral CCG (supracallosal) bundle; bilateral CST; bilateral ILF; bilateral SLF - parietal bundle (SLFP); bilateral SLF - temporal bundle (SLFT); bilateral uncinate fasciculus (UNC).Using DTI analysis, along with the forceps minor, forceps major, and across tract average, we examined FDM using the average of 8 bilateral white matter tracts, while financial awareness was examined using 16 tracts, 8 per hemisphere. These tracts were derived individually for each participant to enable derivation of mean FA and MD within each tract. Specifically, the software performs informed automatic tractography by incorporating anatomical information from a training data set, provided by the software, with the anatomical segmentation of the T1-weighted image of the current data set, thus increasing the accuracy of the white matter tract placement for each participant. Standard DTI processing steps using the FMRIB's Diffusion Toolbox (FMRIB's Software Library v. 4.1.5) including eddy current correction, tensor estimation, and bedpostx were performed prior to tractography. See Yendiki et al. (2011a, 2011b) for detailed steps performed by the TRACULA software. For each participant, the means of FA and MD for each of the 18 tracts were entered into subsequent analyses. Using factor analysis, axial and radial diffusivity metrics were found to be highly correlated to FA and MD, and the four DTI metrics formed two independent factors (unpublished data; also see Gazes et al., 2020). FA ranges from 0 to 1 with higher number representing more intact white matter integrity whereas lower MD values are consistent with more intact white matter integrity.

2.7 Data analysisData were analyzed using IBM SPSS v.25. The data were checked for skewness and negatively skewed data were square root transformed (Field, 2013). Any given demographic variable was used as a covariate only if it was associated with the two variables of interest in Pearson correlations. To understand the association between financial awareness and white matter integrity at any given level of FDM, the latter was included as a covariate if it was related to both variables. Given the hypothesis-driven nature of the correlations, the association between FDM, financial awareness, and white matter metrics were not adjusted for multiple comparisons. Moreover, given that this is the first study to investigate these associations, all the findings have been reported for future replicability and reproducibility of the findings.

3 RESULTSSee Table 1 for the demographic details. Overall, one participant was excluded because of new information about a psychiatric diagnosis, one was excluded because data for FDM were not collected, white matter metrics data were unavailable for nine participants, and financial awareness data were not collected for five participants. In total, 49 participants were included in the FDM analysis and 44 in the financial awareness analyses.

TABLE 1. Demographics characteristics of the sample Mean (SD; range) Age 68.43 (5.14; 57–80) Education (years) 15.88 (2.41; 12–22) Women, n (%) 29 (59) Race, n (%) White 33 (67) Black 14 (29) Asian 1 (2) Native Hawaiian/Pacific Islander 1 (2) Ethnicity, n (%) Hispanic 3 (6) 3.1 Selection of covariates 3.1.1 DemographicsFDM was associated only with education (r = .528, p < .001). However, none of the white matter tract metrics (FA or MD) was associated with education. Age was associated with white matter tracts (see supplementary table) but not with either FDM or financial awareness. Financial awareness was not associated with any other demographics. Therefore, correlations examining white matter in relation to the financial variables were not demographically adjusted.

3.1.2 Financial variablesFDM was associated with financial awareness (r = −.618, p < .001). Therefore, correlations examining white matter metrics in relation to financial awareness were adjusted for FDM only if it was also associated with these metrics (see results below).

3.2 Financial decision-making and white matter integrityFDM was associated with both FA and MD (see Table 2; Figure 1). For FA, FDM was positively associated with ATR (r = .301, p = .036). For MD, FDM showed the strongest negative associations with SLFT (r = −.360, p = .011) and SLFP (r = −.351, p = .014), followed by ILF (r = −.313, p = .030) and ATR (r = −.305, p = .033). The associations between age and these white matter tracts were nonsignificant (r ranged from .012 to .169).

TABLE 2. Associations between financial decision-making and white matter integrity Financial decision-making FA* MD* r p r p N Across tract average .241 .095 −.294a .040 49 Forceps major −.100 .496 .012 .937 49 Forceps minor .012 .936 −.077 .599 49 Anterior thalamic radiation .301a .036 −.305a .033 49 Cingulum - angular (infracallosal) bundle .188 .195 −.057 .699 49 Cingulum - cingulate gyrus (supracallosal) bundle .103 .482 −.039 .791 49 Corticospinal tract .232 .108 −.157 .281 49 Inferior longitudinal fasciculus .223 .129 −.313a .030 48 Superior longitudinal fasciculus - parietal bundle .224 .121 −.351a .014 49 Superior longitudinal fasciculus - temporal bundle .262 .068 −.360a .011 49 Uncinate fasciculus .146 .315 −.168 .249 49

White matter tracts associated with financial decision-making. ATR, anterior thalamic radiation; ILF, inferior longitudinal fasciculus; SLFP, superior longitudinal fasciculus - parietal bundle; SLFT, superior longitudinal fasciculus - temporal bundle

3.3 Financial awareness and white matter integrityTable 3 depicts the associations between financial awareness and white matter integrity (see Figure 2 for the tracts with significant associations). For FA, significant association was observed between financial awareness and left SLFT (r = −.319, p = .035) and it was marginally significant for left ATR (r = −.288, p = .058). Several associations in the case of the MD metric were identified, with the four strongest associations between financial awareness and right SLFP (r = .437, p = .003), right SLFT (r = .433, p = .003), followed by left ATR (r = .391, p = .009) and left ILF (r = .383, p = .010). After adjusting for FDM, only the association between financial awareness and right SLFT (r = .310, p = .046) was significant; while it was marginally significant between financial awareness and right SLFP (r = .296, p = .057). The associations between age and these white matter tracts were nonsignificant (r ranged from −.03 to .13).

TABLE 3. Associations between financial awareness and white matter integrity Financial awareness FA* MD* r p r p N Forceps major .071 .646 −.084 .587 44 Forceps minor .111 .473 .002 .989 44 Left anterior thalamic radiation −.288 .058 .391b .009 44 Left cingulum - angular (infracallosal) bundle −.131 .396 .087 .573 44 Left cingulum - cingulate gyrus (supracallosal) bundle .076 .625 .017 .911 44 Left corticospinal tract −.109 .480 .201 .190 44 Left inferior longitudinal fasciculus −.085 .582 .383a .010 44 Left superior longitudinal fasciculus - parietal bundle −.186 .227 .341a .024 44 Left superior longitudinal fasciculus - temporal bundle −.319a .035 .352a .019 44 Left uncinate fasciculus −.096 .536 .214 .162 44 Right anterior thalamic radiation −.242 .114 .362a .016 44 Right cingulum - angular (infracallosal) bundle −.032 .835 .033 .834 44 Right cingulum - cingulate gyrus (supracallosal) bundle .103 .508 .222 .147 44 Right corticospinal tract −.095 .538 .350a .020 44 Right inferior longitudinal fasciculus −.126 .420 .299 .051 43 Right superior longitudinal fasciculus - parietal bundle −.190 .218 .437b .003 44 Right superior longitudinal fasciculus - temporal bundle −.158 .306 .433b .003 44 Right uncinate fasciculus −.092 .554 .116 .455 44 Across tract average −.172 .265 .269 .078 44 aindicates p < .05 bindicates p < .01

White matter tracts associated with financial awareness. ATR, anterior thalamic radiation; CST, corticospinal tract; ILF, inferior longitudinal fasciculus; SLFP, superior longitudinal fasciculus - parietal bundle; SLFT, superior longitudinal fasciculus - temporal bundle

4 DISCUSSIONTo our knowledge, this is the first study to examine the association of white matter integrity with FDM and awareness of one's financial abilities in older adults without dementia. A key, albeit preliminary finding from this study, is that integrity measures of long-range fibers, especially those connecting frontal–temporal regions were most strongly associated with both FDM and financial awareness. The ATR and the ILF fibers were also consistently associated with both FDM and financial awareness. Importantly, the right SLF tracts, connecting temporal–frontal and parietal–frontal regions, were uniquely associated with financial awareness after adjusting for FDM itself.

Interestingly, while both FA and MD measures were associated with FDM and financial awareness, relatively more associations were noted when white matter integrity was measured using the MD metric. This finding resonates with the results from a large epidemiological examination of brain measures across a wide age range demonstrating that MD declines by 2 SDs relative to age 45 twenty years earlier than FA (Vinke et al.,

留言 (0)